Credit Card Processing

All Credit Card Processing Articles

Expert guides, reviews, and comparisons

ISO Agent vs Direct Processor: Know Who You're Actually Signing With

Learn who actually holds your merchant account when you sign through an ISO or agent. Protect your business by...

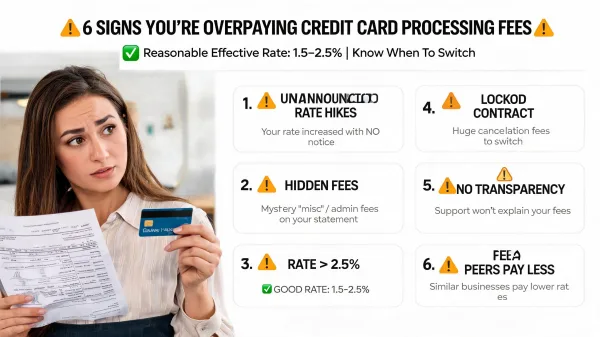

Warning Signs You're Being Overcharged on Processing

Six warning signs reveal whether you're overpaying on credit card processing fees. Learn what reasonable effective...

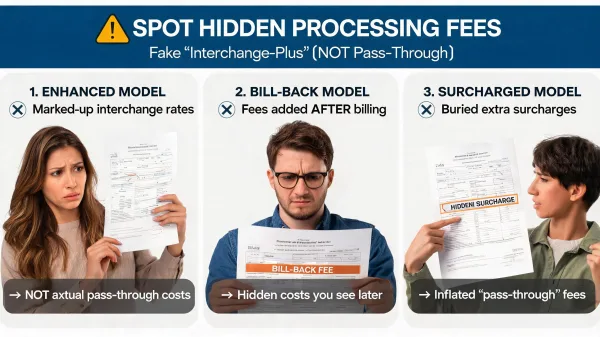

Tiered Pricing Disguised as Interchange-Plus

Some processors sell interchange-plus pricing that isn't actually pass-through. Learn to spot enhanced, bill-back, and...

Junk Fees on Processing Statements and How to Remove Them

Learn to spot merchant services junk fees on your processing statement and get them removed. Covers every common charge...

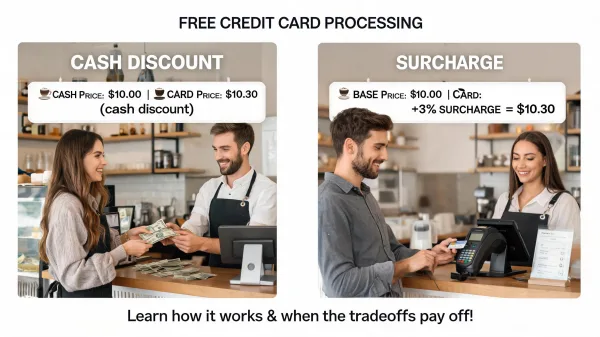

The "Free Credit Card Processing" Claim: What It Really Means

Free credit card processing shifts fees to your customers through surcharging or cash discounts. Learn how it really...

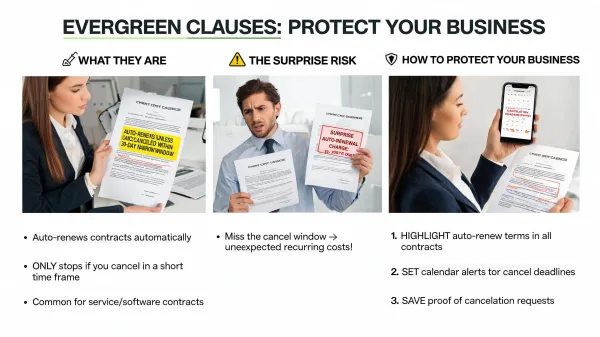

Auto-Renewal Traps in Processing Contracts

Processing contracts often auto-renew unless you cancel within a narrow window. Learn how evergreen clauses work and...

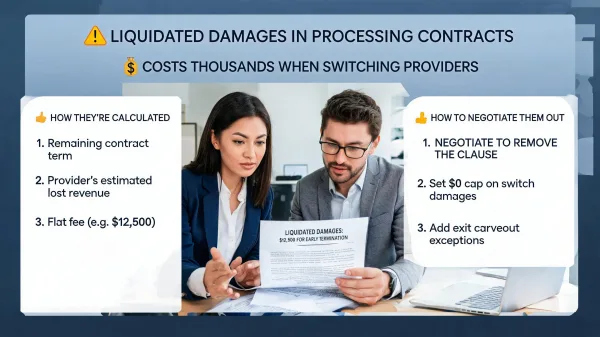

Liquidated Damages Clauses in Processing Contracts

Liquidated damages clauses in processing contracts can cost thousands when you switch providers. Learn how they're...

Early Termination Fees: How to Negotiate Them Out

Credit card processing early termination fees are negotiable. Learn the three ETF structures, pre-signing negotiation...

Equipment Leasing vs Buying: The Real Cost Difference

A merchant services equipment lease can cost $2,400 to $5,760 for a terminal worth $300 to $600. Here is how the real...

Red Flags in a Merchant Services Contract

Learn which merchant services contract clauses trap businesses into costly agreements. Covers auto-renewal traps,...

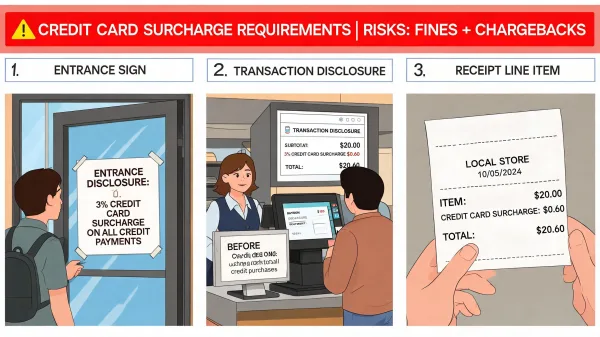

Surcharge Disclosure and Signage Requirements

Credit card surcharge signage requirements cover entrance signs, transaction disclosure, and receipt line items....

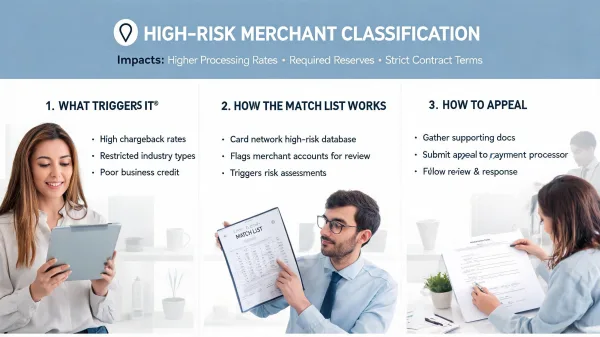

High-Risk Merchant Classification: Criteria and Appeal

High-risk merchant classification affects processing rates, reserves, and contract terms. Learn what triggers it, how...