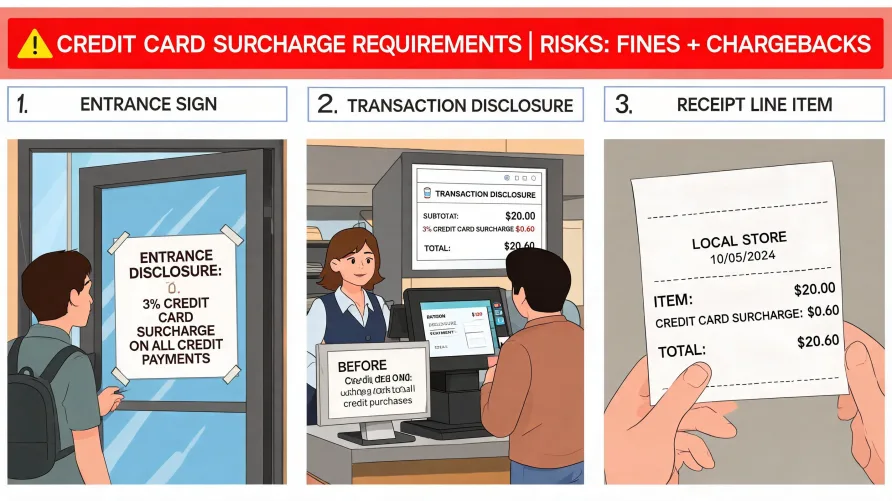

Surcharge Disclosure and Signage Requirements Businesses that add a surcharge to credit card transactions must meet specific credit card surcharge signage requirements set by the card networks and, in many cases, reinforced by state law. Visa and Mastercard both require clear disclosure at three points: where customers enter the business, where the transaction happens, and on the receipt itself. Failing to follow these rules can result in fines, increased chargeback exposure, and removal from the card network's surcharge program. The requirements aren't optional additions to a surcharge strategy. They're the legal and contractual foundation that makes surcharging permissible in the first place. Registering With the Card Networks Before You Surcharge Before any signage goes up or any surcharge appears on a receipt, the merchant must formally register with the card networks. Visa requires at least 30 days' written notice to your acquiring bank before you begin surcharging. Mastercard requires notification through your acquirer as well, though the specific timeline and process may differ. This registration step isn't a formality you can skip and fix later. Merchants who surcharge without completing registration are in violation of their merchant agreement from day one, and the card networks can and do enforce penalties retroactively. Registration also locks in certain parameters. You'll declare whether you're applying a brand-level surcharge (applied to all credit card transactions from a given network) or a product-level surcharge (applied only to specific card types, like premium rewards cards). That distinction matters for signage, because the disclosure language changes depending on which surcharge model you've chosen. Once registered, you're bound to the model you selected. Switching from brand-level to product-level, or vice versa, typically requires a new registration cycle. Two additional constraints apply universally. Surcharges can't exceed 3% of the transaction total under current Visa rules, and they can't be applied to debit card transactions regardless of how the card is processed. If a customer uses a debit card and runs it as credit, the surcharge still doesn't apply. Getting this wrong is one of the fastest paths to a network compliance violation. Credit Card Surcharge Signage Requirements at the Point of Entry The first disclosure obligation kicks in before the customer even reaches the register. Both Visa and Mastercard require that a clearly visible sign be posted at every entrance to the business. For brick-and-mortar locations, that means the front door, any secondary customer entrances, and in some cases, drive-through windows or service counters that function as separate entry points. The sign must state that a surcharge will be applied to credit card transactions. It needs to specify the percentage amount. Vague language like "a small fee may apply" doesn't meet the standard. The sign should clearly identify the surcharge percentage and indicate that it applies to credit card payments specifically, not all card payments. If you're running a product-level surcharge, the sign must identify which card products carry the surcharge. For e-commerce businesses, point-of-entry disclosure translates to the first page where a customer would reasonably begin the checkout process. That could be a shopping cart page, a dedicated payment information page, or a banner on the product page itself if checkout is initiated there. The principle is the same: the customer must encounter the surcharge disclosure before they're committed to the transaction. What the Disclosure Must Actually Say Card network rules don't prescribe exact wording for surcharge signage, but they do set minimum content requirements. At a minimum, the sign must communicate three things: that a surcharge is being applied, that it applies to credit card transactions specifically, and the exact percentage of the surcharge. A compliant sign at a physical location might read something like: "We apply a surcharge of up to 3% on credit card transactions. This surcharge is not applied to debit card transactions." That last sentence matters. Because debit cards are exempt from surcharging, your signage should make the distinction clear. Customers who see a surcharge notice without the debit exemption may assume all card payments are affected, which creates confusion at the register and increases the likelihood of disputes. Some states impose additional language requirements beyond what the networks mandate. Colorado, for example, requires merchants to disclose the surcharge amount and to post the total price inclusive of the surcharge or display both the base price and the surcharge-adjusted price. Merchants operating in multiple states should verify disclosure language requirements in each jurisdiction, because a sign that's compliant in one state may fall short in another. Surcharge Disclosure Rules at the Point of Transaction Meeting the signage requirement at the entrance isn't enough on its own. A second disclosure must occur at the point of transaction, which means at the register, the payment terminal, or the online checkout confirmation screen. This is the moment where the customer is actively completing their purchase, and they need to see or hear that a surcharge is about to be added before the charge is processed. In a physical store, this can take several forms. A printed notice at the register, a message displayed on the payment terminal screen, or a verbal notification from the cashier all satisfy the requirement. The key is timing. The disclosure must happen before the card is charged. A surcharge that appears only after the transaction is processed violates the network rules and gives the customer grounds for a chargeback. Online, the point-of-transaction disclosure typically appears on the payment confirmation page, after the customer has entered their card information but before they click the final "Place Order" or "Confirm Payment" button. The surcharge amount should be displayed as a separate line item at this stage, not buried in a terms-of-service link or hidden in fine print. Surcharge Receipt Disclosure and Line-Item Rules The third and final layer of required disclosure is the receipt. Both Visa and Mastercard require that the surcharge appear as a separate, clearly labeled line item on every receipt where a surcharge was charged. The surcharge amount must be broken out from the transaction subtotal so the customer can see exactly what they're paying for the product or service and what they're paying as a surcharge. This applies to both printed and digital receipts. The line item should be labeled in plain language, something like "Credit Card Surcharge" or "Card Surcharge," and it should show the dollar amount, not just the percentage. Some point-of-sale systems handle this automatically once the surcharge is configured, but merchants should verify that receipts actually display the required information before going live. A receipt that rolls the surcharge into the total without a separate line item doesn't meet the standard. That's true even if the customer was told about the surcharge verbally at checkout. The receipt serves as the permanent record of the transaction, and the networks treat it as a critical compliance artifact. State Laws That Add to the Base Requirements Card network rules establish the floor for surcharge disclosure, but state laws can raise it. As of this writing, a handful of states either restrict or outright prohibit credit card surcharging. Connecticut and Massachusetts currently ban the practice entirely. Puerto Rico also prohibits surcharges. In states where surcharging is legal, additional disclosure or signage obligations may apply on top of the network rules. Colorado's surcharge law is among the most specific. It requires that the surcharge be disclosed before the transaction and that the total price, including the surcharge, be visible to the customer before they agree to pay. New York resolved years of legal ambiguity around its surcharge law through court rulings, and the current framework permits surcharging as long as the total price is clearly communicated. The specifics continue to evolve through legislation and case law in multiple states. Merchants who operate across state lines, whether through e-commerce or multi-location operations, face a patchwork of requirements. The safest approach is to build your disclosure practices around the most restrictive jurisdiction you serve. That way, you're compliant everywhere rather than maintaining different signage and receipt configurations for different markets. Consequences of Non-Compliant Surcharge Disclosure The penalties for failing to meet surcharge disclosure rules aren't theoretical. Visa's surcharge compliance program allows for fines starting at $1,000 per violation and escalating with repeat offenses. Mastercard has similar enforcement mechanisms. Beyond direct fines, non-compliant surcharging increases chargeback risk significantly. A customer who wasn't properly notified about a surcharge has a strong case for disputing the charge, and the merchant will almost certainly lose that dispute. Repeated violations can result in termination from the surcharge program entirely, meaning the merchant loses the ability to surcharge at all. In extreme cases, continued non-compliance can affect the merchant's broader processing relationship, leading to higher processing rates, reserve requirements, or account termination. State-level enforcement adds another layer. State attorneys general have pursued merchants for deceptive pricing practices related to undisclosed or improperly disclosed surcharges. These actions can result in civil penalties, mandatory refunds, and injunctive orders requiring changes to business practices. Building a Compliant Surcharge Disclosure Program The requirements aren't complex individually, but they demand consistency across every customer touchpoint. Registration comes first. Signage goes up at every entry point. Disclosure happens again at the transaction itself. The receipt documents it all. Each layer reinforces the others, and skipping any single step creates exposure. For businesses considering a surcharge program or reviewing an existing one, the card network surcharge rules documentation from Visa and Mastercard is the authoritative starting point. State attorney general websites publish jurisdiction-specific requirements that may add to the network baseline. Getting the disclosure framework right from the beginning costs far less than correcting violations after the fact.

Surcharge Disclosure and Signage Requirements