Where Payment Processing Meets Global Infrastructure

Somewhere between a payment processor and a piece of global commerce infrastructure, Global Payments (NYSE: GPN) occupies a category that most businesses never need — until they do. The Atlanta-based Fortune 500 company scores 8.0 out of 10 in our credit card processing evaluation, a number that reflects an exceptional technology footprint paired with real trade-offs around pricing transparency and support accessibility. For the right organization, those trade-offs are worth making. For many others, they aren't.

Global Payments traces its roots to National Data Corporation's payments and eCommerce division, which became a standalone public company in 2001 as NDC's payments operations separated from what became NDCHealth, the healthcare division. The company accelerated through acquisitions, most significantly merging with TSYS (Total System Services) in a $21.5 billion deal in 2019 — a transaction that added issuer processing, card services, and substantial international infrastructure to an already large merchant acquiring operation. Headquartered in Atlanta, the company employs roughly 27,000 people across 38 countries. In January 2026, it completed a major strategic repositioning: acquiring Worldpay (a deal announced at roughly $24.25 billion headline value, approximately $22.7 billion net after tax assets) while simultaneously divesting its Issuer Solutions business to FIS for $13.5 billion. The result is a company now focused exclusively on merchant commerce — processing $3.7 trillion in annual payment volume across more than 6 million merchant locations globally.

The Technology Underneath

What Global Payments actually delivers to merchants is a combination of payment processing infrastructure, point-of-sale technology, and commerce software — all built to operate at a scale that self-service processors can't replicate. The company processes in 175+ countries, supports multiple currencies and payment methods, and provides local acquiring relationships in key markets rather than routing everything through a single offshore entity. That distinction matters for multinational businesses that need consistent approval rates and local compliance across markets, not just a payment gateway that technically accepts foreign cards.

The core payment stack handles in-person, online, and mobile commerce from a single relationship. EMV compliance, multi-tender support (cards, digital wallets, ACH where applicable), and fully integrated settlement are standard. For businesses operating across multiple locations, the reporting and back-office architecture provides centralized visibility that matters when you're managing dozens or hundreds of payment environments simultaneously rather than one storefront at a time.

Integration depth is a meaningful differentiator. Global Payments provides developer APIs and embedded payment tools aimed at independent software vendors (ISVs) that want to build payment acceptance into vertical software platforms. This is how many businesses encounter the company — through a restaurant management system, healthcare billing platform, or campus commerce solution that has payment processing baked in through a GPN partnership rather than a direct merchant relationship.

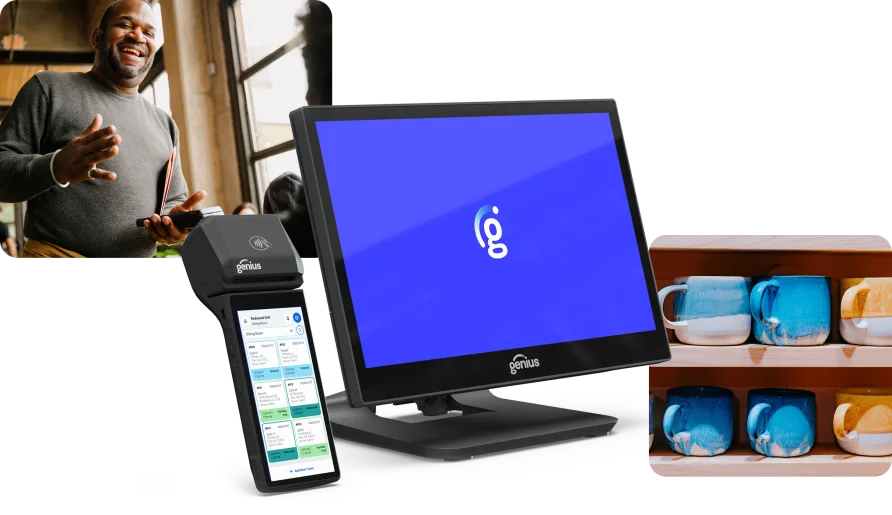

Genius: What the New Platform Changes

The most significant product development in recent memory is the Genius POS platform, which Global Payments began rolling out in May 2025. Genius consolidates more than 16 existing point-of-sale products into a single, modern commerce platform — a necessary move given the company's history of growth through acquisition had left it operating a fragmented portfolio of tools that often competed internally for the same merchant segments.

The platform launched first for restaurants in May 2025, followed by retail in June, enterprise foodservice in September, and higher education in October. By Q3 2025, CEO Cameron Bready reported that in markets where Genius had launched, sales to new merchant locations increased more than 20% year over year, with monthly recurring revenue from new Genius sales rising 75% between June and September. The average deal size more than doubled during the same window. Those metrics point to genuine early traction — particularly among merchants that had been waiting for a unified alternative to GPN's historically fragmented product lineup.

For enterprise foodservice specifically, Genius delivers POS, kitchen management, drive-through automation, digital menu boards, kiosk ordering, and loyalty integration in a single platform. Campuses and stadiums get centralized transaction visibility, compliance controls, and back-office reconciliation across dozens of simultaneous commerce points. In November 2025, Global Payments introduced the first modular, countertop hardware device purpose-built for Genius — designed to adapt from a single-screen terminal to a full dual-display checkout experience without swapping the underlying system.

A UX note worth flagging: merchants moving onto Genius from legacy GPN tools should expect a deliberate migration process rather than an instant cutover. The platform is hardware and OS-agnostic by design, which provides flexibility, but onboarding teams report that configuring the system for complex environments — multi-location quick service chains with regional menu variations, for example — requires more upfront scoping than plug-and-play alternatives. The configurability is genuine; the setup experience reflects that complexity.

Where This Fits Best (and Where It Doesn't)

Consider a regional hospital system processing payments across an outpatient clinic, an affiliated pharmacy, and an online patient billing portal. That organization needs consistent payment infrastructure with HIPAA-aligned data handling, multi-channel settlement, and reporting that consolidates across business units that operate on different billing cycles. Off-the-shelf processors weren't built for that environment. Global Payments was.

The same logic applies to a QSR chain with 200 franchise locations across four countries. Each location needs local acquiring, the franchisor needs consolidated reporting and standardized POS configuration, and the whole system needs to update menu pricing across locations without a manual process at each terminal. Genius for Enterprise targets exactly that operating context.

The picture changes entirely for a business processing under $1 million annually in a single location. That merchant doesn't need multi-currency local acquiring in 38 countries. They don't benefit from dedicated enterprise account management. What they need is transparent pricing, fast setup, and a support line that answers. Global Payments isn't structured to serve that buyer well, and some of the more negative merchant feedback visible in the market comes from smaller operators who reached the company through ISV channel relationships — where they received a GPN-powered product but didn't have access to the enterprise service model that makes GPN work at its best. Users managing smaller operations through these indirect channels frequently mention difficulty determining which GPN-affiliated brand or support team to contact when issues arise.

Pricing and the Engagement Model

There are no published rates. Global Payments operates on custom pricing across all merchant categories, which means the only way to understand what you'd pay is to engage the sales team directly. For enterprise buyers, that's standard operating procedure — a hospital system or multinational retailer isn't going to pick a payment processor off a pricing page, and the rates negotiated at volume can be materially better than published interchange-plus structures at smaller processors.

For mid-market businesses doing their first serious payment infrastructure evaluation, the lack of benchmarks creates friction. You'll go into the sales conversation without context for whether a proposed rate is competitive. Preparation matters: know your current effective rate (total processing costs divided by total volume), your card mix (debit vs. credit, card-present vs. card-not-present), and your annual volume. With those numbers in hand, you can evaluate any quote against your baseline. Without them, the opaque engagement model puts you at a negotiating disadvantage.

Global Payments' 2024 financials give a sense of the infrastructure behind the relationship: the Merchant Solutions segment posted roughly $7.7 billion in segment revenue, against total company GAAP revenue of $10.1 billion. The company allocates substantial capital to product development — management and coverage have characterized annual R&D-equivalent spending as well into the hundreds of millions. That's a processor with the resources to maintain infrastructure, build new product (Genius being the clearest example), and support complex deployments — but the cost structure behind that investment gets passed into merchant pricing through the custom rate negotiation rather than transparent tier structures.

Where Global Payments Stops

Within the scope of credit card processing, the gaps worth knowing about relate to accessibility rather than capability. There's no self-service account creation, no published interchange-plus or flat-rate pricing, and no instant onboarding path for businesses that need to start accepting payments within days rather than weeks. The entire model is built around relationship-based sales and implementation, which is appropriate at enterprise scale and limiting for everyone else.

The organizational complexity introduced by years of acquisition also creates real navigation challenges. Heartland Payment Systems, TouchNet, and OpenEdge all operate as GPN-affiliated brands serving different market segments. For a merchant who encounters a support issue and isn't sure whether they're a Heartland customer, an OpenEdge merchant, or a direct Global Payments account, finding the right team takes more effort than it should.

Our Assessment

Global Payments is genuinely impressive at what it does — which is process payments at a scale and geographic breadth that very few organizations in the world can match. The Worldpay acquisition, closed January 9, 2026, adds further scale: 6 million merchant locations and $3.7 trillion in annual volume make the combined entity one of the two or three largest merchant acquirers on the planet. The Genius platform rollout shows a company that's willing to do difficult internal consolidation work rather than let a fragmented product portfolio erode its competitive position.

The 7.7 score reflects those real strengths alongside the trade-offs that come with an enterprise-first model. Pricing opacity, support complexity across a multi-brand structure, and an onboarding experience designed for deliberate implementation rather than fast activation are all real limitations. They're appropriate limitations for the market this company serves — but they're limitations nonetheless. If your organization has the transaction volume, the multi-market footprint, or the vertical complexity that makes an enterprise payment partner necessary, Global Payments belongs in your evaluation. If you don't, the fit isn't there, and that's not a criticism — it's just an accurate description of what this product was built to do.