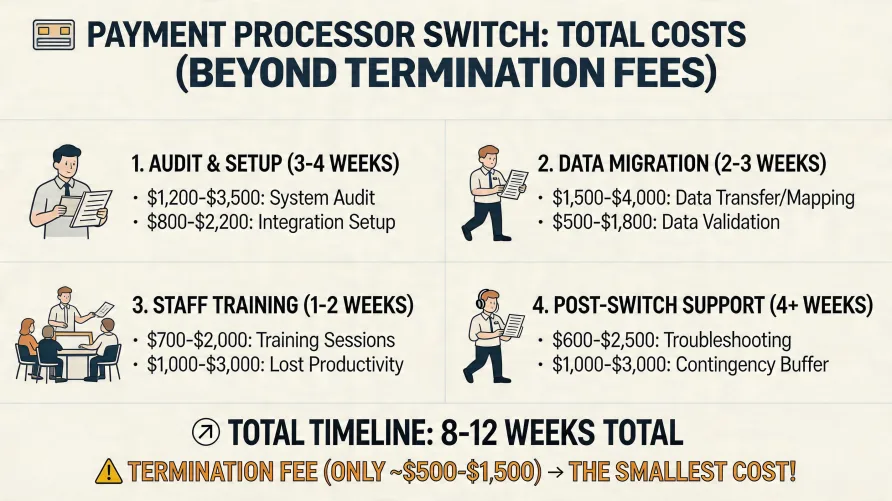

If you're researching the cost to switch payment processor providers, plan for between one and three percent of your annual processing volume in total transition costs, plus three to twelve weeks of partial attention from someone on your team. That's the real answer, not the marketing answer. The early termination fee is usually the smallest line item in the calculation. The expensive parts are the equipment you can't return, the gateway integration nobody scoped, and the recurring revenue you watch decline before your card updater catches up.

I've been through processor migrations as both an operator and a buyer of merchant services for two decades. The pattern repeats. Owners look at the savings on the rate sheet, sign the buyout offer, and discover the actual switching cost in months three through six. This is a breakdown of where that money actually goes, what timelines look like in practice, and the scenarios where the math works out against you.

Early Termination Fees

Yes, there's almost always a fee to switch credit card processors mid-contract. Standard processor agreements include a tiered early termination fee that ranges from $295 to $695 in flat amounts, plus what's called liquidated damages on some contracts. Liquidated damages are calculated as the average monthly fees you would've paid over the remaining contract term. On a three-year contract with two years left and average monthly fees of $400, that adds up to $9,600 on top of the flat ETF.

A handful of states have taken action on opaque ETF clauses in merchant services contracts. State attorneys general have settled cases against processors over deceptive contract auto-renewal, but the underlying ETF structure is still legal in most states. Read the contract before assuming the fee is unenforceable.

Some new processors offer buyout programs that cover ETFs up to a stated cap, often $295 or $500. These offers come with conditions. The buyout usually gets paid as a credit against your first six to twelve months of fees, not as cash, and the new contract typically locks you in for three years with its own ETF schedule. You're trading one cancellation cost for another.

Hardware Replacement, Returns, and Lease Unwinding

This is where I've watched the biggest losses happen. Payment terminals tied to a specific processor can rarely move to a new one. Even when the hardware is technically compatible, the encryption keys are loaded by the original processor and the device often has to be reinjected, reflashed, or replaced outright. If you bought the terminals, you might recover a fraction of cost on resale. If you leased them, you're stuck.

Equipment leases are the cost I see business owners miss most. A typical merchant terminal lease runs 48 months at $39 to $99 per month, non-cancellable, with no buyout provision until the term ends. A fleet of five terminals on a four-year lease at $69 monthly works out to over $16,000 in committed payments. Switching processors doesn't end the lease. The leasing company is a separate entity from the processor, and they'll keep billing you for the full term whether or not the equipment is still plugged in.

If you're evaluating a switch and your hardware is leased, get the lease paperwork in front of you before you do anything else. The early termination fee on the processing contract is a rounding error compared to a stranded equipment lease.

The Gateway and Integration Cost Most Owners Underestimate

Card-present businesses generally have an easier migration than ecommerce or recurring billing operations. If your transactions flow through a gateway, virtual terminal, shopping cart integration, or custom API, that's a redevelopment project, not a configuration change. Standard ecommerce on a supported platform with a connector for the new processor typically runs $500 to $2,500 in plugin costs and developer time. Custom checkout or in-app payment flows built against the old processor's API can take 40 to 120 developer hours to rebuild against the new one. At typical contractor rates that's $5,000 to $20,000 of work before the first transaction clears.

Subscription management and point-of-sale systems are the worst surprise. Subscription billing platforms that work natively with a specific processor may require platform changes or rebuild work, especially when the switch also forces a move off a billing platform exclusive to the old processor. POS software tied to a processor account often won't accept credentials from a competing processor without a software change or, in some cases, a full POS replacement. I've seen restaurants discover this two weeks before their planned cutover date.

Recurring Billing and the Card Updater Problem

This is the cost category that surprises subscription businesses most. When you switch processors, you don't just move tokenized cards from one vault to another. The major card networks operate account updater services, but participation in those services is tied to your merchant account. New account, new participation, new sync window. What that looks like in practice: a portion of your stored card credentials at the old processor were getting refreshed automatically when cards expired or got reissued. After the migration, those refreshed credentials sit at the old processor and your new processor has the stale ones. Decline rates spike for the first two to four months while the new account's updater service catches up with new card data. On a subscription book of $100,000 monthly recurring, even a three percent decline rate increase translates to $3,000 monthly in revenue you have to chase or lose.

There's also a customer notification dimension. Card brand operating rules generally require merchants to give cardholders advance notice of material changes to recurring billing arrangements that include the merchant of record. If your new processor uses a different merchant of record name on the cardholder statement, that's a disclosure event. Failing to handle it cleanly drives chargebacks, which carry their own cost.

Downtime Risk and the Cutover Window

Can you lose sales during a processor switch? Yes, and it's the most preventable cost on this list. Total downtime isn't usually long, often 30 minutes to a few hours during the actual cutover, but partial functionality issues can run for days. Saved cards stop working. Recurring batches fail until they're reconfigured against the new account. Refunds that need to clear through the old processor get tangled because the merchant account is closed.

The professional approach is to run both processors in parallel for two to four weeks. New transactions go to the new processor, and refunds, recurring billing, and customer service issues route through the old one until they're resolved. This costs slightly more in account fees during overlap but eliminates almost all sales loss.

Staff Retraining and the Soft Costs

The reports come out different. The reconciliation workflow your bookkeeper uses changes. The chargeback response process moves to a new portal. The customer service team has to learn new transaction lookup screens. None of this individually is a big number, but it accumulates.

For a small operation with one or two people handling daily merchant operations, plan on 8 to 20 hours of training and procedural updates. For a larger operation with dedicated payment ops, the number climbs to 40 hours or more during the first month after cutover.

How Long Does the Whole Thing Actually Take?

Realistically, 30 to 90 days from signed application to fully migrated operations for a typical small business. Card-present only with no ecommerce or recurring billing? Often three to four weeks. Ecommerce with a custom integration and a subscription book? Closer to eight to twelve weeks, sometimes longer if seasonal volume forces a delay in the cutover window.

Underwriting and account approval is usually two to ten business days, depending on industry risk classification. Hardware ordering, encryption key injection, and shipment is one to three weeks. Gateway integration work and testing depends on complexity, but two to six weeks is the realistic range. The cutover and parallel processing window is typically one to four weeks. Anyone telling you it's a one-week project is selling, not advising.

When Switching Pays Back in Three Months vs Eighteen vs Never

I think about this the same way I think about any operational change. What's the realistic monthly savings, what's the all-in switching cost, and what's the payback window?

Three-month payback scenarios are real but uncommon. They look like a high-volume business processing $200,000 plus per month, currently paying an effective rate of 3.4 percent because of legacy tiered pricing, switching to interchange-plus pricing at an effective 2.6 percent. The 80 basis point savings on $200,000 is $1,600 monthly. If switching costs total $4,800, payback hits in three months.

Eighteen-month payback is the more typical scenario. A moderate-volume business saving 30 to 40 basis points, with $8,000 to $15,000 in switching costs spread across ETF, equipment, and integration work. The math works, but you have to commit to the new processor for at least the payback window plus the new contract term.

The scenarios where switching never pays back happen more often than processors will admit. They look like a low-volume business under $20,000 monthly, where the rate savings are real but small, and the switching costs include a $9,000 stranded equipment lease the new processor's buyout offer doesn't cover. The new monthly rate is better, but you'll pay for the migration over the next thirty months while the lease runs out. In that case, the right answer is often to wait for the lease term to expire and switch then.

The Final Cost Calculation

The actual cost to switch payment processor providers isn't the rate difference times your volume. It's the rate difference times your volume, minus the early termination fee, minus the stranded equipment, minus the integration redevelopment, minus the lost recurring revenue during the updater sync, minus the staff hours, minus the cutover risk. After all that, look at whether the new effective rate beats the old one by enough to justify the disruption.

The right time to switch is usually when your contract is up, your equipment is owned outright or near end of lease, and the savings are large enough to absorb a few months of disruption. Switching mid-contract because a sales rep showed you a lower rate sheet is how owners end up paying more in year one than they save over the next three combined.

If you're looking at providers in this market, the rate sheet is the easiest part of the comparison. The harder part is the contract structure, the equipment terms, and the migration support. Those determine whether your switching cost stays inside the savings or eats them.