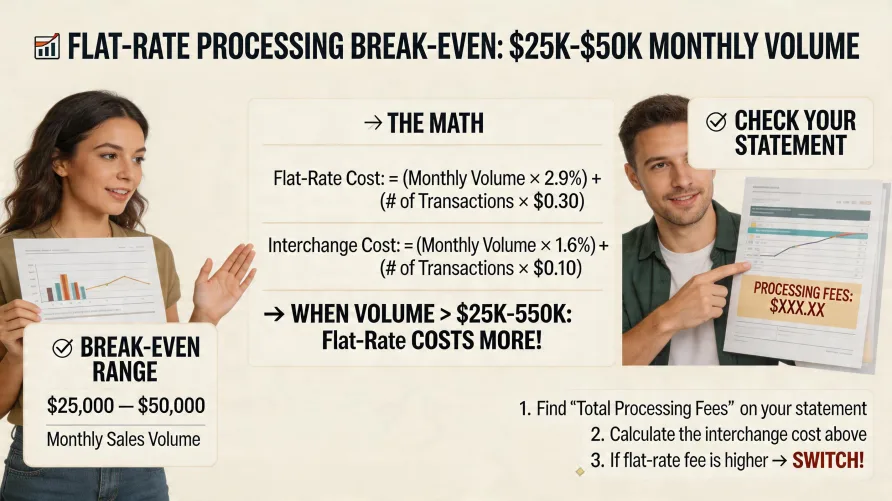

Knowing when to switch from flat-rate processing comes down to a single calculation: at what monthly card volume does interchange-plus save more than enough to justify the switch. The crossover usually lands somewhere between $25,000 and $50,000 in monthly card volume, though the real break-even depends on your card mix, average ticket size, and how much of your business runs in person versus online. I've watched dozens of growing businesses overpay for years because they kept the same processor that worked when they were doing $5,000 a month. The arithmetic that made flat-rate cheap then is the same arithmetic that makes it expensive now. The Two Pricing Models, Stripped Down A flat-rate aggregator charges one published rate on every transaction, regardless of what that card actually costs to accept. The pricing looks like 2.6% plus 10 cents in person or 2.9% plus 30 cents online. You know what each sale will cost before it happens. That predictability is why flat-rate works for new businesses. There's no statement to interpret and no monthly fee structure to manage. An interchange-plus processor splits the same transaction into two parts: the underlying interchange fee set by the card networks, plus a markup that goes to the processor. Interchange itself isn't a single rate. It's a published table that varies by card type, transaction method, and merchant category. A regulated debit card from a large bank can cost as little as 0.05% plus 22 cents under the Durbin Amendment cap, per Federal Reserve published data. A premium rewards credit card swiped in person might cost 2.10% plus 10 cents. The processor adds something on top of that, often 0.10% plus 5 cents to 0.40% plus 10 cents, sometimes with a monthly account fee in the mix. Why Flat-Rate Wins at Low Volume The math favors flat-rate when your absolute savings can't overcome the monthly fees and the time cost of managing a more complex statement. If your effective flat-rate is 2.85% and an interchange-plus alternative gets you to 2.55% effective, that's 30 basis points of savings. On $5,000 of monthly volume, that's $15. On $10,000, it's $30. Most interchange-plus accounts have monthly fees, statement fees, PCI compliance fees, or some combination that totals $20 to $60 a month. At those volumes, you're trading predictability for marginal savings or no savings at all. There's a soft cost too. A flat-rate dashboard tells you what you paid in one number. An interchange-plus statement breaks each transaction into interchange, assessment, network fees, and processor markup. The first time you read one, it can take an hour to verify it's accurate. That hour matters more when your business is small. When to Switch From Flat-Rate Processing: Volume Scenarios Here's how the picture changes as volume grows. These are scenarios I've worked through with operators in different industries, using realistic effective rates rather than rate-card best cases. $10,000 a month, card-present retail You're paying roughly $260 a month under flat-rate. An interchange-plus account on the same volume might bring processing costs down to $230, then add $25 in monthly fees. You save about $5. The switch isn't worth the operational headache. $25,000 a month, mixed-channel coffee shop Flat-rate runs around $725 a month. Interchange-plus could land you at $620 in processing plus $25 in fees, so $645 total. You save about $80 a month, $960 a year. That's now real money, but you're still close to the line if your ticket size is small. Per-transaction fees on either model add up fast when your average sale is under $8. $50,000 a month, professional services with rewards-heavy card mix Flat-rate at 2.9% plus 30 cents online comes in around $1,450 plus per-transaction fees. Interchange-plus on the same business often lands at $1,200 to $1,250 all-in. You're saving $200 to $250 a month, $2,400 to $3,000 a year. The switch pays for itself many times over. $100,000 a month, B2B with corporate card volume This is where the math gets ugly for flat-rate. Corporate and purchasing cards carry higher interchange rates, but a flat-rate processor charges the same 2.9% on a corporate card costing them 2.4% in interchange as it charges on a regulated debit card costing them 0.30%. You might pay $2,900 a month under flat-rate when interchange-plus would put you at $2,300 to $2,500. That's $400 to $600 a month, or up to $7,200 a year. Variables That Move the Flat-Rate vs Interchange-Plus Crossover Volume isn't the only thing that determines when flat-rate stops paying off. Four factors push the crossover point earlier or later. Card-present versus card-not-present mix Online and keyed-in transactions carry higher interchange than swiped or dipped cards. If you're 100% e-commerce, your true cost of acceptance is higher, which means flat-rate is closer to actual interchange and the savings from switching shrink. If you're 100% in-store retail with chip readers, your true cost is lower and flat-rate is leaving more money on the table. Average ticket size Per-transaction fees matter more on small tickets. A 10-cent fee on a $4 coffee is 2.5% on its own. On a $400 invoice, the same 10-cent fee is 0.025%. Small-ticket businesses hit the crossover later because the fixed-cost part of the fee dominates the percentage. High-ticket businesses hit it sooner. Card mix Rewards cards, business cards, and corporate cards carry higher interchange than basic consumer credit and especially regulated debit. If your customers tend to use premium rewards or business cards, flat-rate is subsidizing your processor more heavily. If your mix skews toward debit cards from large banks, which are capped under the Durbin Amendment, the gap is smaller. Industry category code The card networks publish reduced interchange rates for certain merchant types: utilities, charities, education, supermarkets, and a few others. If you're in one of those categories, the gap between flat-rate and interchange-plus is wider, because flat-rate doesn't pass those reduced rates through to you. Signs You're Outgrowing Flat-Rate Processing Outgrowing flat-rate processing usually announces itself in your monthly P&L before you notice it elsewhere. Your processing line gets bigger faster than your revenue line. Your effective rate creeps up as your card mix shifts toward more rewards cards and corporate cards. You start asking why a $50 sale costs you $1.75 to accept when the bank that issued the card charged your processor 80 cents. If your monthly card volume has roughly tripled since you set up your current account, that's the moment to run the numbers. The right answer at $5,000 a month is rarely the right answer at $25,000, and almost never the right answer above $50,000. When Flat-Rate Still Makes Sense at Volume Flat-rate doesn't always lose at $50,000 or $100,000 a month. There are situations where it keeps making sense. If you have very small average tickets and high transaction counts, the per-transaction component of either pricing model can wash out the percentage difference, particularly when your average ticket sits below $10. If your card mix is debit-heavy and Durbin-capped, your true interchange is so low that flat-rate's percentage doesn't hurt as much, and the headline 2.6% rate is closer to your actual blended cost. If your finance team can't absorb the operational complexity of reading interchange statements every month, the time cost can offset the rate-sheet savings. If your business has frequent disputes or fraud concerns and your current processor handles those well, the relationship value matters more than the marginal basis points you'd pick up. There are also operators who simply prefer the budget predictability that flat-rate gives them and would rather pay a known premium than chase variable savings. I've seen operators stay on flat-rate at $200,000 a month and not be wrong about it. They knew what they'd save, they knew what they'd give up, and they made the trade with eyes open. The Switching Costs You Might Not See The published savings from a switch quote are rarely the savings you keep. Real switching cost shows up in places that don't appear in the comparison sheet. Hardware and integration If you're moving off a flat-rate provider that gave you free terminals or a self-contained app, you may need to buy or lease new hardware. Integration with your point-of-sale, e-commerce platform, accounting system, or invoicing tool may require developer time or new plugins. Verify your existing software supports the new processor before you sign anything. Underwriting time A flat-rate aggregator brings you live in minutes. An interchange-plus processor underwrites the merchant the way a bank underwrites a loan. Approval can take a few days for low-risk businesses or a few weeks for higher-risk ones, with documentation requests along the way. If you can't take a downtime hit, plan the switch carefully. Contract terms and termination Some interchange-plus processors offer month-to-month accounts. Others bundle three-year contracts with early termination fees that can run into four figures. Read the merchant agreement before signing, especially the section on auto-renewal and price-increase clauses. Reserve requirements Higher-risk merchants, including subscription businesses, ticketing, travel, and certain service categories, may face a rolling reserve on an interchange-plus account that didn't exist on the flat-rate platform. This can tie up working capital you didn't plan to lose. Running the Numbers: When to Switch From Flat-Rate Processing You don't need a sales rep to figure out whether you're overpaying. Pull your last three months of merchant statements and do the math yourself. First, find your effective rate. Add up your total processing fees for the month and divide by your total card volume. If you processed $40,000 and paid $1,160 in fees, your effective rate is 2.90%. Do this for three months and average them. Second, estimate what you'd pay on interchange-plus. The card networks publish their interchange rate cards, and the Federal Reserve publishes data on average debit interchange under the Durbin cap. For a typical SMB mix, your blended interchange will land somewhere between 1.7% and 2.3% depending on your channel, ticket size, and card mix. Add a markup of 0.20% to 0.40% for the processor. Then add monthly fees of $20 to $60 across processing, statement, PCI compliance, and gateway charges where applicable. Third, compare. If your annualized savings exceed $1,500 to $2,000 after fees, the switch is usually worth it. Below that, the operational disruption may eat the gain. A Final Word on Quoting the Market The decision to leave flat-rate isn't a one-and-done conversation. Even after switching, your effective rate will drift over time as your card mix changes, your transaction volume grows, and your processor's markup adjusts during contract renewals. I quote my own processing every 18 to 24 months whether I think I'm overpaying or not. The exercise itself surfaces things I'd missed: a fee that crept up, a tier I'd outgrown, a piece of hardware I was renting at four times its purchase price. For a sense of how providers in this market compare on transparency, contract structure, and pricing model at different volume levels, see the credit card processing reviews and ranking page.

When Flat-Rate Stops Saving You Money