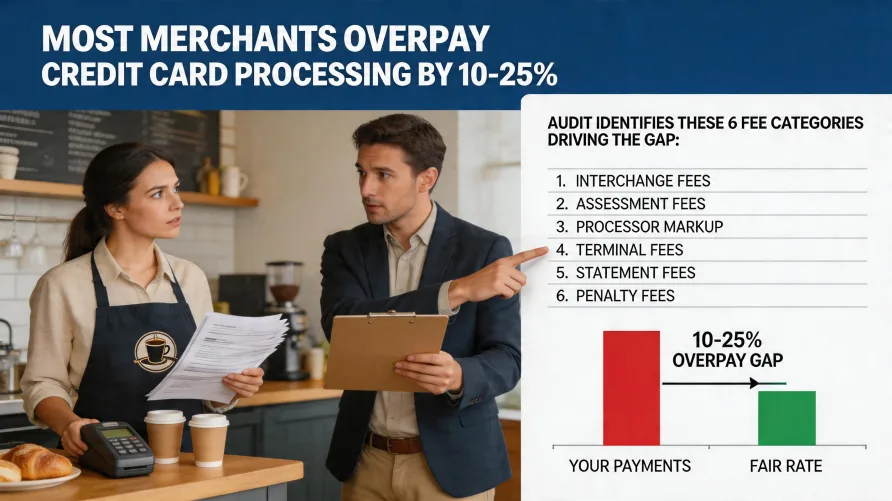

After hundreds of merchant statements have crossed my desk over the years, six categories of overcharges keep showing up regardless of which processor wrote the contract. A credit card processing audit is the line-by-line review that finds them, and most merchants who run one are paying somewhere between 10 and 25 percent more than they need to. The audit reads the fee schedule, the actual interchange data, and the contract together to expose the gap between what's owed and what's billed. What a Merchant Statement Audit Is A merchant statement audit reads three documents together: the monthly processing statement, the original merchant agreement and fee schedule, and the published interchange tables from the card networks. A surface read of the statement shows totals and rate categories. A real processing fee audit checks whether each individual line item is justified by the contract, whether the interchange categories assigned to each transaction look right for the card type and ticket size, and whether any fee on the statement has no contractual basis at all. The third item happens more often than people expect, especially after a contract has been in place for two or three years. The work isn't glamorous. It's the kind of thing most business owners would rather not spend a Saturday on. But the recovery is usually proportional to the time invested. Where Credit Card Processing Audits Find Money Padded Interchange Pass-Through Interchange-plus pricing is supposed to mean the merchant pays the network's published interchange rate plus a fixed markup. In practice, the "interchange" line on the statement isn't always the published rate. Some processors quietly add a few basis points to the pass-through and then label the inflated number as interchange. The contracted markup sits on top of the inflated base. The merchant ends up paying the contracted markup plus a hidden second markup buried inside a line item that's supposed to be a direct cost. Catching this requires comparing each transaction's interchange charge against the network's published schedule for that card type and category. When the numbers don't line up, the gap is the padding. The gap doesn't surface unless someone runs the math. Inflated Tiered Pricing Downgrades Tiered pricing buckets transactions into qualified, mid-qualified, and non-qualified rates. The qualified rate is what gets advertised. The non-qualified rate is often two to three times higher. The mechanic that drives most of the overcharging is in how transactions get sorted. A processor on a tiered model has discretion over which bucket each transaction lands in, and the contract often doesn't bind that discretion to any specific interchange category. Rewards cards, corporate cards, keyed-in transactions, and a long list of other situations get pushed into non-qualified for reasons that have nothing to do with cost. An audit pulls the transaction-level data and flags downgrades that don't match the underlying interchange. The savings here can be steep, especially for businesses that take a lot of rewards cards or corporate cards. Monthly Fees That Don't Belong A typical statement carries a stack of monthly fees: statement fees, account fees, gateway fees, batch fees, IRS reporting fees, monthly minimums, customer service fees. Some are legitimate. Most have a contractual basis, even if the basis is buried in a fee schedule the merchant never read. But two patterns repeat. First, new fees get added after the contract is signed, sometimes with notice that goes into the statement footer where nobody reads it. Second, fees keep getting charged after the service they're attached to has been canceled or replaced. An audit catches both. The recovery on this category alone often runs $50 to $200 a month for small merchants. Junk Compliance and Regulatory Fees These show up under names like "regulatory compliance fee," "industry compliance fee," "annual compliance fee," or "card brand assessment recovery." Some recover real costs the processor pays to the networks. Others don't. A small number are pure invention with no underlying assessment behind them. The audit work here is verifying that any fee labeled as a regulatory or compliance pass-through actually corresponds to a published assessment from a network or regulator. When it doesn't, the fee has no defensible basis. When the line item shows up after a contract change rather than at signing, the case for refunding it gets stronger. PCI Fees That Shouldn't Apply PCI compliance is a real requirement set by the Payment Card Industry Security Standards Council. Merchants are typically responsible for completing an annual self-assessment questionnaire or attestation depending on their volume tier and processing method. Processors charge two related things in this area. The first is a PCI compliance program fee, which covers the processor's tools and reporting resources. The second is a PCI non-compliance fee, which is supposed to apply only when the merchant hasn't completed and submitted a current attestation. In practice, non-compliance fees keep getting charged to merchants who are fully compliant, often because the processor lost the attestation, never asked for it, or never updated the merchant's status after the attestation was submitted. Recovering twelve months of non-compliance fees on a merchant who was actually compliant is a regular audit finding, and the refund is one of the easier ones to document. Equipment Lease Overcharges This one produces the biggest single-line savings figures. A countertop terminal that retails for around $300 to $500 gets leased to a small business for $39 to $89 per month over four or five years on a non-cancellable lease. The math comes out to thousands of dollars for hardware that cost a few hundred. Worse, the lease is often a separate contract held by a leasing company, not the processor, so canceling the processing agreement doesn't end the lease payments. Court records in several states show consistent patterns of merchant complaints against equipment leasing companies in this market, and some state attorneys general have brought enforcement actions against the more aggressive operators. Lease terms and merchant remedies vary by state. An audit identifies these contracts and quantifies the cost. Getting out of the lease is a separate fight. The first step is knowing the cost is there. Can You Audit Your Own Processing Statement? Yes, partially. Any business owner can pull the last twelve months of statements and start looking for repeating fees, fees that appeared mid-contract, and rate categories that don't match what was promised. A spreadsheet, the original contract, and an afternoon will surface the obvious overcharges. What a self-audit can't easily do is verify interchange against the published network schedules at the transaction level. That work requires either the raw transaction-level batch data, which most processors don't volunteer, or specialized tools that benchmark statement-level interchange against network norms. For things like duplicate fees, surprise monthly charges, and PCI non-compliance fees on a compliant account, a self-audit catches a lot. For padded interchange pass-through and tiered downgrade abuse, the work usually needs an outside reviewer with the right tools. How Much a Processing Audit Actually Saves The realistic answer: it depends on how big the problems are and how much volume the business runs. A merchant doing $30,000 a month on a tiered pricing plan with an equipment lease and unchecked PCI fees can typically recover $200 to $600 a month in ongoing savings, sometimes more. A merchant on a clean interchange-plus contract with no equipment lease and a current PCI attestation might find very little. The pattern in my experience is that businesses with monthly volume under $500,000 often have at least 10 percent of their effective processing cost tied up in fees that wouldn't survive scrutiny. Common merchant account audit findings cluster into the same six categories described above, in some combination, with equipment leases and PCI non-compliance charges driving the largest single-line recoveries. The recovery isn't always immediate cash. It's often a combination of refunds for past charges and lower forward rates after the contract gets renegotiated or replaced. Free Audits vs Independent Audits The merchant statement audit market has two distinct types of providers and they aren't doing the same job. The first type is the free audit offered by a competing processor or sales agent. It's a sales tool. The reviewer's incentive is to find enough wrong with the current statement to justify a switch. Sometimes the analysis is real and the criticism is fair. Often the savings claim depends on a new contract that introduces its own version of the problems being criticized, just under different line item names. The conflict of interest doesn't make the analysis worthless, but it means the conclusions need a second look from someone who isn't selling anything. The second type is an independent paid audit from a consultant who isn't selling processing services. The fee structure varies. Some charge a flat hourly or project rate. Others charge a contingency, typically 25 to 50 percent of documented savings over a defined period. The independent model has its own incentive issues, especially on contingency work where the auditor has reason to inflate findings. The absence of a downstream sales pitch still matters. When the audit finds nothing, an independent reviewer says so. A free audit from a competing processor almost never reaches that conclusion. When a Credit Card Processing Audit Pays Off Run an audit when the effective rate on the statement is above 3 percent, when the contract is more than two years old, when an equipment lease is in place, when monthly statements include line items with vague names, or when the business has never done one. The cost of a paid independent audit is usually a few hundred to a few thousand dollars depending on volume and complexity. The recovery, when there's something to find, almost always covers the cost many times over. For businesses evaluating providers in this market, an audit produces something useful beyond direct savings: a clear-eyed view of what a fair processing relationship actually costs, which is the only baseline that matters when comparing options.

What a Processing Audit Actually Finds