Credit Card Processing Designed for B2B Workflows

Most companies that accept B2B credit card processing payments are overpaying on every transaction without realizing it. The reason isn't the rate they negotiated. It's the data their system sends with each transaction. When a payment goes through with only basic card information, card networks classify it as Level 1, the highest-risk and most expensive processing tier. EBizCharge exists to solve that specific problem, and it does so by embedding payment processing directly into the ERP and accounting systems where B2B transactions already live. We score EBizCharge 7.1 out of 10 for the credit card processing category.

The platform is built by Century Business Solutions, a privately held company founded in 2004 and headquartered in Irvine, California. What started as a merchant processing company evolved into a hybrid operation: part payment processor, part software developer. The company reports more than 400,000 users across the U.S. and Canada and processes billions in annual transaction volume. It's remained privately held throughout its history, which it credits for keeping its focus on product development rather than investor returns. The entire team is in-house, including the software development and customer support departments.

How Level 2 and Level 3 Data Cuts B2B Processing Costs

The core value proposition of EBizCharge is interchange optimization through enhanced transaction data. Credit card networks like Visa and Mastercard assign interchange rates based partly on how much information accompanies a transaction. Level 1 processing, the default for most setups, includes only the basics: card number, transaction amount, and merchant details. Level 2 adds tax amounts, invoice numbers, and customer codes. Level 3 goes further, requiring nearly twenty fields of line-item detail including item descriptions, quantities, unit costs, freight charges, and commodity codes.

The difference in cost isn't trivial. B2B transactions processed at Level 3 can qualify for interchange rates that are 0.5% to 1.0% lower per transaction than Level 1 rates. On a $15,000 invoice paid with a corporate purchasing card, that's $75 to $150 in savings on a single transaction. Multiply that across a year's worth of B2B receivables and the numbers become significant. EBizCharge automates this data capture by pulling invoice details directly from your accounting or ERP system. You don't manually enter twenty extra fields per transaction. The integration handles it.

Many government and purchasing card programs expect Level 3 line-item data for best interchange qualification, and in some cases, for acceptance itself. That means government vendors often don't have a practical choice about whether to pursue this capability. But any company accepting corporate purchasing cards, fleet cards, or business credit cards can benefit from the same interchange reductions. The catch is that your payment system has to actually capture and transmit the enhanced data correctly, and most generic processors don't.

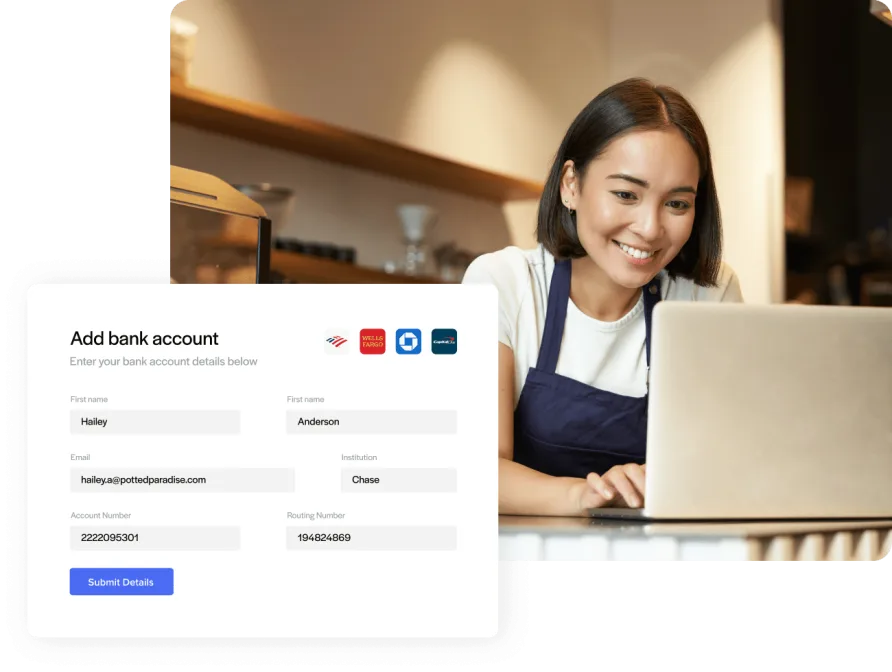

ERP Integration as the Core Product

EBizCharge integrates natively with over 100 ERP, CRM, accounting, and eCommerce platforms. That list includes QuickBooks (Desktop and Online), Sage (50, 100, 500, Intacct, BusinessWorks), SAP Business One, Microsoft Dynamics (GP, Business Central, Finance and Operations), NetSuite, Epicor (9, 10, Kinetic), Acumatica, Oracle EBS, Salesforce, and dozens more. The integrations aren't surface-level API connections. They're built to work inside the existing ERP interface, so your accounting team processes payments without leaving the software they already use.

This matters for two reasons. First, it eliminates double data entry. When a payment is processed through EBizCharge, it automatically posts to the general ledger and accounts receivable in the ERP system. No one re-keys a transaction from a separate terminal. Second, the integration is what enables Level 2 and Level 3 data capture. Because EBizCharge lives inside the ERP, it can pull invoice line items, tax amounts, shipping details, and customer reference numbers directly from the source data. That's the mechanism that qualifies transactions for lower interchange tiers. Without the ERP connection, you'd need to enter all that data manually for every transaction, which almost nobody does consistently. The automation also reduces the risk of data entry errors that can cause interchange downgrades, where a transaction that should have qualified for Level 3 rates gets bumped back to Level 1 because a required field was missing or formatted incorrectly. Those downgrades cost real money, and they tend to go unnoticed until someone audits the processing statements months later.

Beyond processing, the platform includes a suite of accounts receivable tools. The customer payment portal lets your clients log in to a branded web interface, view outstanding invoices, and pay online with stored payment methods. Email pay generates payment links from inside your accounting software. Auto-pay rules can charge stored cards on file automatically on a set schedule. Recurring billing handles repeat charges. All of these sync back to the ERP without manual intervention. Users managing accounts receivable for mid-size distribution companies report that these tools cut their manual collection effort substantially, with some citing reductions from 30-day average collection times to under a week.

What EBizCharge Costs in Practice

EBizCharge doesn't publish its processing rates. All pricing is custom-quoted based on transaction volume, average ticket size, and which ERP integration you need. This is common among B2B-focused processors, but it makes comparison shopping harder than it should be. You can't pull up a pricing page and compare rates against another provider without first going through a sales conversation.

The company markets interchange-plus pricing, which means your rate consists of the base interchange fee set by the card networks plus EBizCharge's markup. They also highlight that all features, integrations, and support come standard with a merchant account, with no separate software licensing fees. That's a relevant distinction because some competitors charge monthly SaaS fees on top of processing rates for their ERP plugins. EBizCharge also advertises no setup fees and no cancellation fees, though you'll want to confirm those terms in writing during the quoting process.

The real cost calculation for EBizCharge is less about the stated rate and more about the effective rate after Level 2 and Level 3 qualification. If your current processor charges you 2.8% on a $10,000 B2B invoice processed at Level 1, and EBizCharge can get that same transaction qualified at Level 3 with a rate closer to 2.0%, you're saving $80 per transaction. A company processing $100,000 per month in B2B card payments at that differential would save roughly $9,600 annually in interchange costs alone. That math only works if your transaction mix actually includes corporate, purchasing, or government cards that qualify for enhanced data rates. Standard consumer credit card transactions won't see the same benefit.

Who Gets the Most from EBizCharge

The ideal EBizCharge customer looks like this: a wholesale distributor running SAP Business One, processing $50,000 to $500,000 per month in B2B credit card payments from corporate purchasing cards, currently watching interchange fees eat into margins because their existing processor sends every transaction at Level 1. That company has an ERP system already in place, a defined accounts receivable workflow, and enough B2B card volume that a 0.5% to 1.0% per-transaction reduction in interchange translates to real annual savings.

Government vendors are another strong fit. If you sell goods or services to federal, state, or local agencies that pay with GSA or purchasing cards, Level 3 processing is often expected and sometimes required. EBizCharge automates the line-item detail those transactions need, which eliminates the manual data entry that makes government card acceptance painful for many vendors.

The fit weakens in a few scenarios. A retail shop processing mostly consumer Visa and Mastercard swipes won't benefit from Level 2/3 optimization because consumer cards don't qualify for enhanced data rates. A startup without an ERP or accounting system loses the integration advantage entirely, and the standalone virtual terminal, while functional, doesn't differentiate EBizCharge from dozens of other processors. Companies processing primarily international transactions will also find the U.S. and Canada limitation restrictive.

The Gaps to Know About

Pricing transparency is the most obvious gap. Every other aspect of the product is well-documented on the website, but the complete absence of any published rate, benchmark, or even a pricing range makes initial evaluation slow. You can't assess whether EBizCharge fits your budget without scheduling a call.

The reporting tools have room to grow. In our evaluation, bulk report exporting doesn't always support preferred formats, and historical transaction lookups can slow noticeably under heavy load. These aren't dealbreakers, but they add friction for accounting teams that depend on clean, fast reporting workflows during month-end close or audit prep.

Support runs through direct outreach rather than a structured ticketing portal. If your team handles multiple ERP environments or needs to track open issues across departments, confirm the support workflow and escalation process during onboarding. The support staff themselves are well-regarded, but the infrastructure around issue tracking could use an upgrade.

Geographic reach is limited. EBizCharge is a registered Independent Sales Organization (ISO) of Wells Fargo, PNC Bank, Pathward, and Synovus in the U.S., plus Wells Fargo's Canadian branch and U.S. Bank's Canadian operations. If your business processes transactions in Europe, Asia, or Latin America, you'll need a different processor for those markets.

Recent Platform Developments

In January 2026, EBizCharge launched embedded payment applications for Infor CloudSuite Distribution (CSD) and Infor CloudSuite Industrial (CSI), expanding its ERP integration library into a platform widely used by manufacturers, wholesalers, and distributors. The Infor integration follows the same native approach as its other ERP connections, allowing users to process credit, debit, and ACH payments without leaving the Infor environment.

The company's award trajectory has accelerated. In 2025 alone, EBizCharge received a Grand Stevie Award for Highest-Rated New Product, two Gold Stevie Awards, three People's Choice Stevie Awards, two Gold Globee Awards, and an Inc. 5000 listing for the sixth time. It also earned a USA TODAY Top Workplace designation. While awards don't replace product evaluation, the volume and consistency of recognition across multiple judging bodies reflects a company investing in both product quality and market positioning.

The Verdict

EBizCharge occupies a narrow but important lane in credit card processing. It's not trying to be everything to everyone. It's built specifically for B2B companies that want to stop overpaying on interchange fees and need their payment processing to live inside the accounting systems they already run. If that describes your operation, the combination of Level 2 and Level 3 data optimization, deep ERP integration, and included AR automation tools makes EBizCharge one of the more compelling options in the B2B credit card processing space. The lack of published pricing is a frustration, and you'll need an ERP system to get the platform's full value. But for the right business with the right transaction mix, the interchange savings alone can justify the switch.