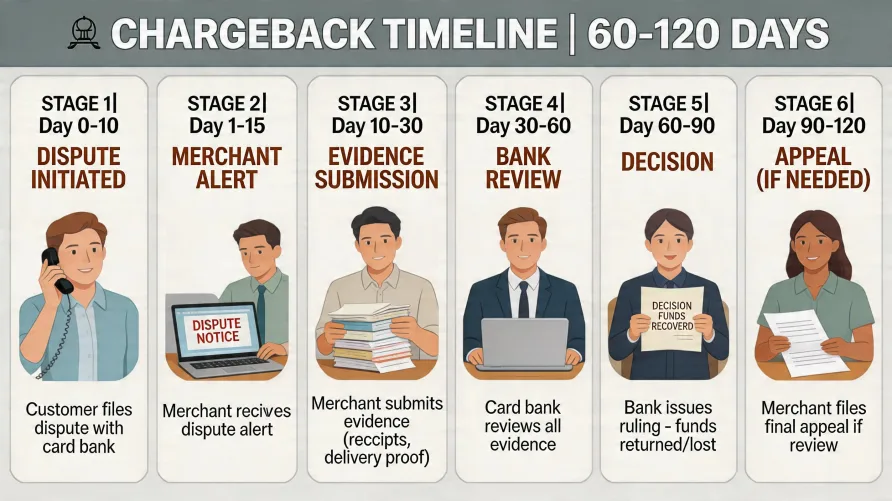

The chargeback dispute process timeline moves through six recognizable stages over roughly 60 to 120 days, and most of those stages run on deadlines that are tighter than merchants expect when they receive their first dispute notice. By the time the chargeback notification lands in your inbox, the customer has usually already had their money returned, a reason code has been assigned, and your response window has started counting down. The window is short. Often 30 days, sometimes 20, occasionally as little as a week for a retrieval request that precedes the formal chargeback. Knowing what happens at each stage and what evidence the issuing bank actually weighs is the difference between recovering disputed revenue and watching it walk out the door. I've been running and advising businesses for more than 20 years, and I can tell you that the merchants who handle chargebacks well aren't smarter than everyone else. They're operating with a clearer picture of the merchant chargeback dispute stages and what each one actually demands. This is that picture, week by week. Week 0: The Customer Files the Dispute The clock starts before you know anything's happening. A cardholder logs into their bank's mobile app, taps "dispute this charge," and answers a few prompts. Fifteen minutes of effort on the customer's side. The issuing bank evaluates the claim and, in most cases, issues a provisional credit. The cardholder has their money back. You haven't been notified yet. This timing matters because it shapes the bank's incentive structure. The issuing bank is your customer's customer. They want to keep the cardholder happy. The bank funds the provisional credit out of its own pocket and then attempts to recover from your acquirer. That recovery is the chargeback you'll soon hear about. Cardholders typically have 60 to 120 days from the transaction date to file most disputes, and some categories stretch longer. Services not provided can run as long as 540 days under one major card brand's published rules, and recurring billing complaints have their own timing. By the time a slow-moving customer disputes a six-month-old charge, you may have already shipped, fulfilled, refunded, or moved on. The issuer doesn't care. The window's still open under the rules. Week 1: Sometimes a Retrieval Request, Sometimes Not Before the formal chargeback hits, some disputes start with a retrieval request. This is a request for documentation. The issuer wants to see the receipt, the signature, the delivery proof, anything that confirms the charge happened the way you say it did. You typically have 7 to 15 business days to respond, depending on the card brand and the type of request. Modern dispute systems have reduced the use of retrieval requests for many reason codes. The current Visa dispute resolution framework, for example, routes most fraud claims directly to chargeback rather than passing through a retrieval stage first. For some categories, including certain billing disputes, the retrieval request still appears. If you ignore it, the dispute escalates automatically into a chargeback. That's the worst possible outcome at this stage. The retrieval request is your cheap shot at resolving the issue before money moves. Week 1 to 2: The Chargeback Notification Lands Your processor sends the notice. The funds have already been debited from your merchant account. The reason code is attached to the notice, and the reason code is the most important piece of information you'll receive in this entire process. It tells you what the cardholder is claiming, what the issuer needs you to prove, and how much chance you have of winning the case. Reason codes fall into broad families across the major networks: fraud, authorization, processing errors, consumer disputes, and miscellaneous. Each family treats evidence differently, and reading the code correctly on day one will shape every action that follows. Reason Codes That Favor the Merchant Authorization and processing-error codes are the most winnable. If the cardholder is disputing a transaction that has clean authorization, an AVS match, a CVV match, and a clear processing trail, the documentary case writes itself. The same applies to "cardholder doesn't recognize" claims, which often dissolve once the merchant submits transaction history showing the customer has used the same card at the business before. Card-present fraud claims are also generally favorable to merchants who followed liability shift rules. EMV chip transactions read at a chip-capable terminal protect the merchant under the 2015 liability shift framework. If a chip was inserted and the transaction was processed correctly, the issuer typically owns the loss for counterfeit fraud. Reason Codes That Favor the Cardholder Card-absent fraud is harder. When a customer claims their card number was used without authorization in an online or phone transaction, the merchant carries the burden of proof, and "we processed the order" isn't enough. The issuer wants delivery confirmation matching the cardholder's billing address, IP address geolocation that lines up with the cardholder, and ideally prior transaction history establishing the relationship. "Services not as described" and "merchandise not received" claims also tilt toward cardholders by default. The cardholder's word that they didn't receive what they paid for carries weight unless the merchant can produce shipping proof tied to the cardholder's address with delivery confirmation, or a signed delivery receipt for goods over a certain dollar threshold. Subscription cancellation complaints are a growing category, and they almost always go to the cardholder unless the merchant can show explicit, recent acknowledgment of the recurring billing terms. A buried "by signing up you agree to recurring billing" clause from three years ago usually won't hold up in dispute review. Weeks 2 to 4: The Representment Window Once the chargeback is logged, you have the right to dispute it back. This is called representment, and the chargeback representment timeline depends on the card brand. Current as of writing: Visa allows 30 calendar days from the chargeback processing date. Mastercard allows 45 calendar days. American Express typically allows 20 days for most disputes. Discover allows 30 days. These deadlines are firm. Miss them and you forfeit the dispute. The clock starts when the chargeback is processed by the network, not when your processor forwards the notification to you, which means an extra few days can disappear between when the deadline started running and when you found out about it. Build a 48-hour internal SLA for processing every chargeback notification the day it arrives. What Evidence Actually Wins This is where merchants either recover the money or don't. The compelling evidence package is what the representment will rise or fall on. Evidence that wins: Shipping proof with delivery confirmation tied to the cardholder's billing address, ideally with signature for purchases above a meaningful dollar threshold. If the package was signed for at the same address on file with the issuer, the cardholder's "I never got it" claim collapses. AVS and CVV match data on the original authorization. These data points sit in your processor's records and can be pulled for the dispute response. Prior transaction history showing the cardholder used the same card at your business previously. Six prior successful transactions with the same card at the same merchant tells a strong story about whether this seventh transaction was really fraudulent. Communication logs and policy acknowledgments. If the customer agreed to terms in a way that produced a record (clicked a checkbox, signed a contract, replied to a confirmation email), include the record. Terms of service the cardholder agreed to at the point of purchase. Not buried in a footer. Acknowledged at checkout. Evidence that doesn't win: A screenshot of your refund policy with no proof the customer saw it. A generic order confirmation email with no delivery proof. The phrase "we delivered the product" with no documentation behind it. A chronology of customer interactions that doesn't include the cardholder's own words. Internal notes from your customer service team without the customer's responses. The issuer is reading the evidence package on a clock too. Their reviewer has minutes, not hours. Your case has to be obvious. Weeks 6 to 8: The Decision The issuer reviews the representment package and rules. If they rule in your favor, the funds are returned to your merchant account, often net of any chargeback fees the processor charged when the case opened. Those fees aren't always refunded. If the issuer rules against you, the chargeback stands. You've now lost the disputed amount, the chargeback fee, and the processing time you spent on the case. You have one more option, and it gets expensive. Weeks 8 to 12: Pre-Arbitration Pre-arbitration is the merchant's last informal chance to escalate. You're saying to the issuer: I have new evidence, or you misread the case, and I want you to look again before this goes to formal arbitration. The deadline to file pre-arbitration is typically 30 days from the representment decision, sometimes shorter under specific reason codes. Pre-arbitration requires new evidence. You can't just resubmit the same case. If the issuer accepts your pre-arbitration, the case is reversed in your favor without going further. If they reject it, you face a decision about arbitration. Beyond Week 12: Arbitration Arbitration is the card network making the final call. Filing fees range from roughly $250 to over $500 per case depending on the network, and the loser pays. For a disputed transaction under $200, arbitration almost never makes economic sense. For larger transactions, or for cases where the same fact pattern is showing up repeatedly and you want a network-level ruling, it can be worth pursuing. Most merchants stop at representment. The math on arbitration is brutal for typical card-present and small-ticket card-absent disputes. Deadlines at a Glance The full chargeback timeline, from the moment a customer files to a final ruling, breaks down to a handful of windows you should know cold: Cardholder filing window: 60 to 120 days from transaction (longer for some categories, current as of writing). Retrieval request response: 7 to 15 business days, when applicable. Representment: 20 to 45 days depending on card brand. Pre-arbitration: typically 30 days from the representment decision. Arbitration: the card network sets the schedule, typically resolved within 60 to 90 days of filing. The full lifecycle from initial dispute to arbitration ruling can stretch past six months. Most cases resolve within 90 days at representment. What I've Learned About Chargebacks I've watched chargebacks shape merchant relationships with their processors more than almost any other operational issue, and the pressure builds in tiers most owners don't see until they're inside one. A chargeback rate above 1% triggers monitoring programs at the major card networks. Above 1.5%, you're in remediation status, and your processor will start applying reserves or asking you to find a new home. The economics of every transaction change once you cross those thresholds, and the changes compound. Reserves tie up working capital. Higher per-transaction fees show up at the next pricing review. New processor relationships become harder to open because your merchant history follows you. The harder truth underneath all of this is that the system isn't built to be fair to merchants. It's built to protect cardholders, who are the card brands' real customers in a consumer-driven business. Friendly fraud, where customers buy something, receive it, and dispute the charge anyway, is the fastest-growing category of chargebacks I've watched develop in the past five years. What I tell other merchants: the chargeback you win is good, but the chargeback you prevent is better. Federal Reserve Payments Study reporting and CFPB consumer complaint patterns both reflect rising friendly-fraud volume, and that's the kind of dispute almost no representment package can recover. Clear product descriptions, billing descriptors that actually identify your business on bank statements, fast and visible refund processing, and proactive customer communication will reduce dispute volume more than any representment skill ever will. Once a customer has filed with their bank, you've already lost the trust contest. The dispute is a recovery operation, not a relationship. Where to Go From Here If you're evaluating providers in this market, the GuidingDecisions Credit Card Processing ranking page covers options across the spectrum, from flat-rate aggregators to traditional processors with deeper compliance support. Each has its own approach to dispute management, fee structures, and merchant tools. The right fit depends on your transaction profile, your industry's chargeback baseline, and how much risk you're willing to absorb in exchange for convenience. A first chargeback feels like a setback. It's actually a calibration event. Use it to understand what your business looks like to an issuing bank, what your evidence trail looks like under pressure, and where the gaps are. That's the most expensive lesson you'll get for free.

A Chargeback Dispute Timeline: Week by Week