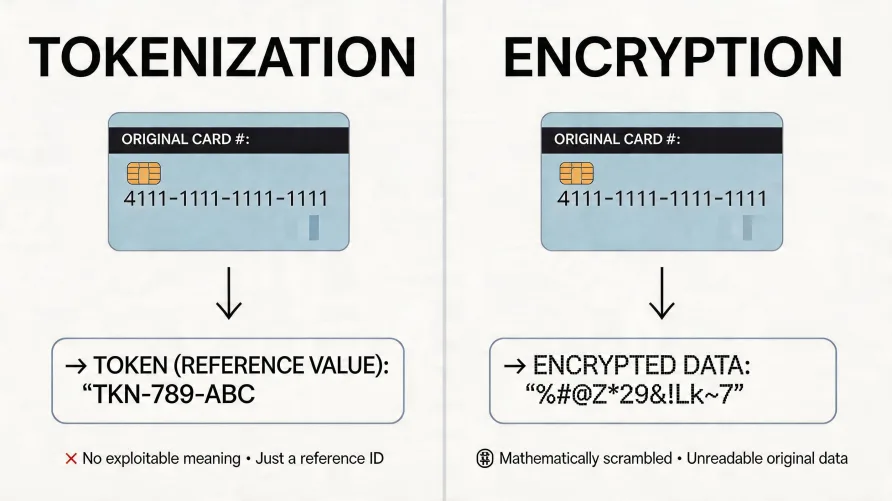

For payment processing, tokenization and encryption protect card data in different ways and at different points in the transaction flow. Encryption scrambles the actual card number using a mathematical algorithm so it can't be read without the corresponding key. Tokenization replaces the card number entirely with a meaningless reference value that has no mathematical relationship to the original. Modern payment processing uses both in combination, not one instead of the other. Understanding which technology protects which segment of the transaction is what separates merchants who actually understand their PCI obligations from those who assume their processor handles security automatically. What Payment Tokenization Actually Does Tokenization replaces a primary account number, or PAN, with a substitute value called a token that holds no exploitable information. According to the PCI Security Standards Council, a token by itself must be useless to an attacker who steals it. The original PAN is stored in a tightly controlled vault, often operated by the payment processor or a dedicated tokenization service, and the token is what gets passed around through the merchant's systems instead. This matters because PCI DSS scope is determined by where cardholder data lives. If a merchant's database stores tokens rather than card numbers, that database falls outside the high-risk scope of the standard. The PCI SSC has explicitly recognized tokenization as a method that can reduce scope, provided the token can't be reverse-engineered to recover the PAN and the tokenization solution is properly implemented and segmented. Tokens can be format-preserving, matching the length and structure of a card number for legacy systems, or fully randomized. They can be single-use, scoped to a specific merchant, or reusable for recurring billing. The flexibility is what makes tokenization useful as a working substitute for the PAN in everyday business operations like refunds, recurring charges, and transaction lookups, all without the merchant ever holding the real card number. How Card Data Encryption Works in Payments Encryption converts card data into ciphertext using a cryptographic algorithm and a key. AES-256 is the current industry standard for symmetric encryption, and asymmetric variants handle the secure exchange of keys between parties. The protection is mathematical. Without the correct key, the ciphertext is statistically meaningless. In payments, encryption happens at multiple layers. Data in transit between the customer's browser and the merchant's checkout page is protected by TLS. Data on a card-present terminal is encrypted at the read head, before it ever touches the merchant's point-of-sale software. Data at rest in databases, backups, and log files is typically protected by storage-level encryption. The weakness of encryption isn't the math. It's the keys. Anywhere the key exists, the data can be decrypted. That includes memory during processing, hardware security modules, and the systems of any party authorized to decrypt the payload. An attacker who steals encrypted data along with the key has stolen the data outright. This is why key management practices matter as much as the encryption algorithm itself. PCI DSS requires that encryption keys be generated, distributed, stored, rotated, and retired under documented procedures, with split knowledge and dual control for the most sensitive operations. A merchant who deploys strong encryption but stores the key in the same database as the encrypted data has effectively undone the protection. Tokenization vs Encryption in the Payment Stack A clear way to think about this: encryption protects card data while it moves and while it sits at rest, and tokenization replaces card data so the merchant doesn't have to keep moving or storing it. The first time a card number enters the system, at the swipe, dip, tap, or keystroke, the data must exist in its original form for at least an instant. Encryption protects that moment. Once the card has been authorized and the merchant needs a reference for future use such as recurring billing, returns, or loyalty matching, tokenization lets the merchant keep working with the customer's account without keeping the actual PAN. This division also drives PCI DSS scope reduction. Card data encrypted under a strong algorithm with proper key management is still considered cardholder data within scope, because anyone who possesses the key can read it. A token, properly issued, is not cardholder data and falls out of scope. That's the practical difference. Encryption protects data. Tokenization removes data from the merchant's environment entirely. For merchants choosing how to structure their payment systems, the question isn't whether to use encryption or tokenization. It's how aggressively to push tokenization upstream so the merchant's environment never holds raw PANs at all. Network Tokens vs Processor Tokens Not all tokens are created equally. The distinction between network tokens and processor tokens matters for merchants thinking about long-term card-on-file strategy. Processor tokens are issued by the merchant's payment processor or gateway. They work within that processor's environment and typically don't transfer if the merchant changes processors. The lock-in is real. A merchant with thousands of stored card credentials in processor-specific tokens faces real friction if they later want to switch providers, and the longer the merchant stays on a given processor, the more those tokens accumulate as a soft form of vendor lock-in. Network tokens are issued by the card networks themselves and represent the cardholder's account at the network level. The networks publish their tokenization specifications publicly, and tokens generated under those programs can be used across processors that support them. A network token also updates automatically when the underlying card is reissued, expired, or replaced after fraud, which reduces the rate of failed recurring charges and the abandoned-cart problem caused by expired stored credentials. For merchants running subscription businesses or any operation that relies on stored card credentials, network tokens are usually the better choice. They reduce processor lock-in, improve authorization rates, and shift the maintenance burden of stale card data away from the merchant. Authorization rate improvements alone can be material for high-volume recurring revenue businesses, where a few percentage points of incremental approvals translate to real revenue over time. End-to-End Encryption and P2PE in Payments End-to-end encryption, often abbreviated as E2EE, means card data is encrypted at the point of capture and remains encrypted through every system it touches until it reaches the entity authorized to decrypt it. In a properly implemented payment E2EE setup, the merchant's point-of-sale software, network, and back-end systems never see the unencrypted card number. Point-to-Point Encryption, or P2PE, is the PCI SSC's formal version of this concept. P2PE is a validated standard with a list of approved solutions published by the council. To qualify as P2PE, a solution must encrypt data at a tamper-resistant security module inside the payment terminal, manage decryption keys outside the merchant's environment, and meet specific requirements for hardware, key management, and chain-of-custody auditing. The benefit for merchants is real. A validated P2PE solution dramatically reduces PCI DSS scope for card-present transactions because the merchant's systems never possess decryptable card data. The card-present environment shifts from a major compliance burden to a manageable one. The PCI SSC maintains a public listing of validated P2PE solutions, which merchants can verify when their processor claims P2PE support. Why Modern Payment Processing Combines Tokenization and Encryption Encryption and tokenization solve different problems. That's why production payment systems use them together. When a card is presented at a terminal, P2PE or equivalent encryption protects the data from the read head through the processor. The processor decrypts the payload inside its secured environment, authorizes the transaction, and returns a token to the merchant. From that point forward, the merchant works with the token. Card data was never decryptable on the merchant's side, and now it isn't stored on the merchant's side at all. For online transactions, the pattern is similar. The cardholder's data flows from the browser to a hosted payment field controlled by the processor, encrypted in transit by TLS. The processor returns a token to the merchant. The merchant's web application stores the token, not the card number. The combination is what makes meaningful PCI scope reduction possible. Encryption alone can't remove cardholder data from scope. Tokenization alone can't protect the card during the brief moment it must exist in original form. Together, they do. The question of whether tokenization is better than encryption misses how the two technologies actually relate. Tokenization eliminates the merchant's exposure to card data; encryption protects card data wherever it must still exist. The first reduces what has to be defended, the second defends what's left. Asking which is better is like asking whether a vault is better than an armored truck. They serve different purposes in the same security architecture. Can Tokenized Cards Be Stolen? A token by itself can't be used to make a fraudulent charge against the original card, provided the tokenization is properly implemented. The token has no value outside the system that issued it. If an attacker steals a database of tokens from a merchant's environment, they can't take those tokens to a different merchant and run them as transactions. The risk surface shifts rather than disappearing. The tokenization vault still holds the actual PANs, and that vault is now a high-value target. The networks and processors that operate vaults invest substantial resources in physical and logical security around them. Strong tokenization implementations also bind tokens to specific merchants or use cases, so a stolen token is useful only in the limited environment where it was issued. Tokens can also be misused if the merchant's own systems are compromised in ways that let an attacker submit transactions through the merchant's authenticated channels. That's an authentication and access control problem, not a tokenization weakness. What This Means for Your Merchant Security Posture The practical takeaway for any merchant evaluating their payment infrastructure: confirm that the processor uses both encryption and tokenization, not just one. Ask whether card-present transactions run through a validated P2PE solution. Ask whether stored credentials use network tokens or processor-specific tokens, and what the migration path looks like if the merchant ever changes processors. PCI DSS compliance scope isn't a static condition. A merchant who encrypts card data but stores it in their own database is in scope for nearly every PCI requirement. A merchant who never holds raw card data, because their processor returns tokens for everything and uses P2PE for terminals, has dramatically smaller compliance obligations and a smaller attack surface. The technology to do this properly is widely available. The question for merchants is whether their current processor uses it, and how aggressively. For a survey of providers in this market, see the credit card processing reviews and rankings on this site.

Tokenization vs Encryption: What Actually Protects Card Data