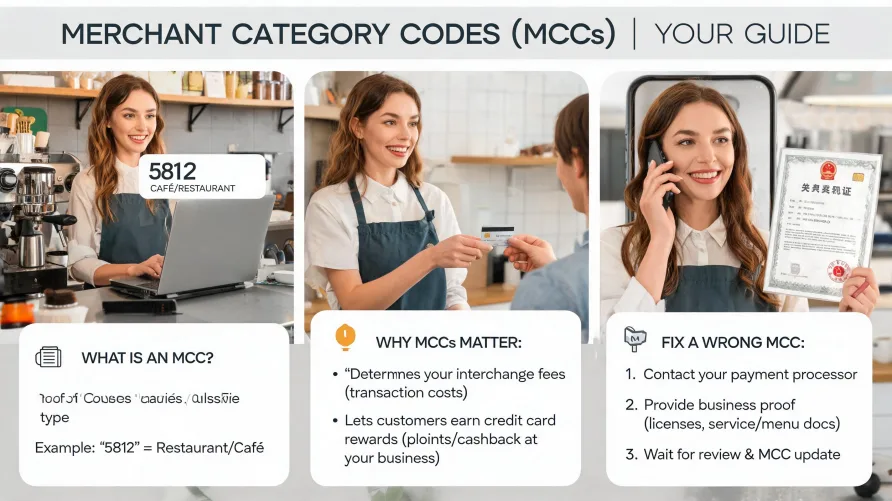

What Is a Merchant Category Code? How Classification Shapes Your Processing Costs A merchant category code is a four-digit number assigned to every business that accepts card payments. It classifies what your business sells or what service it provides, and it directly affects your interchange rates, your customers' rewards eligibility, and whether certain transactions get approved at all. Understanding how your merchant category code works in practical terms is one of the more overlooked pieces of running a card-accepting business. How Merchant Category Codes Work MCC codes exist because card networks need a standardized way to sort millions of merchants into defined business types. The International Organization for Standardization maintains the underlying framework under ISO 18245, which establishes the structure and principles for assigning these codes. Visa, Mastercard, American Express, and Discover each publish their own MCC code list based on that standard, though the lists aren't identical across networks. The differences between network lists are usually minor, covering edge cases or industry-specific subcategories, but they can matter when a merchant falls near a classification boundary. The codes range from 0001 to 9999. A grocery store typically falls under 5411. Legal services land at 8111. Fast food restaurants get 5814. Some codes cover broad industry categories, while others target specific niches. A veterinary clinic receives a different classification than a general medical practice, and a gas station gets a different code than the convenience store sharing its parking lot. Each network's published MCC code list is publicly available. Visa's appears in its Merchant Data Standards manual, and Mastercard publishes its version in the Quick Reference Booklet. These are the authoritative references when questions about classification arise. How Your MCC Code Gets Assigned Your merchant classification code is assigned during the underwriting process, whether you're applying for a traditional merchant account or signing up through a payment facilitator. The acquiring bank or processor reviews your business type, your primary revenue source, and how you described your products or services on your application. Based on that review, they select the MCC that best matches your operation. The assignment isn't always accurate. A business selling both retail goods and repair services might get classified under either code, and the choice pushes interchange rates in different directions. Businesses with mixed revenue streams face the highest risk of misclassification because the underwriter typically picks a single code based on whatever appears to be the primary activity at the time of approval. If your revenue mix shifts over time, your original MCC may no longer reflect what your business actually does, but it won't update automatically. You'd need to request a reclassification. You don't choose your own MCC. That decision sits with the acquiring bank, guided by card network rules and your application materials. Why Your Merchant Category Code Affects Processing Rates Interchange is the fee your acquiring bank pays the cardholder's issuing bank on every card transaction. Card networks set interchange rates using a matrix that factors in card type, transaction method (card-present versus card-not-present), and the merchant's MCC code. Different codes carry different rates, and the differences aren't trivial. Grocery stores and gas stations typically qualify for lower interchange because those categories process high volumes of routine, low-fraud transactions. Restaurants and hotels often face higher rates. Professional services, online retail, and dozens of other categories each sit at their own point on the interchange matrix. According to Federal Reserve data, the average interchange fee for debit card transactions in 2022 was approximately 0.57% of the transaction value, but that average obscures significant variation across merchant categories and card types. Premium rewards cards carry higher interchange than standard debit, and MCC classification determines which rate table applies to your transactions. The gap between categories isn't small. Depending on card network and card type, interchange can vary by 50 to over 100 basis points between merchant classifications. For a business processing $500,000 in annual card volume, that difference translates to several thousand dollars per year in processing costs. That's real money. This is exactly why misclassification carries financial consequences. If your business is coded under a higher-interchange category than your actual activity warrants, you're overpaying on every transaction. How MCC Codes Affect Cardholder Rewards Your customers feel the effects of MCC codes too, even if they don't realize it. When a credit card offers 3% cash back on dining or 5% on groceries, the issuing bank uses MCC codes to determine which purchases qualify for the bonus. A transaction at a business coded as a restaurant (5812) earns the dining reward. The same purchase at a business coded as a caterer (5811) might not. This creates friction that merchants rarely anticipate. If your cafe carries a general retail code instead of a restaurant classification, your customers won't earn their dining rewards when they buy from you. Most won't say anything directly, but some will notice when they review their statement. Issuers don't override MCC assignments to award bonus categories. The code is the code. For businesses competing in categories where card rewards drive customer behavior, an incorrect MCC can quietly erode a competitive advantage. Policy-Based Restrictions and High-Risk MCC Classifications Certain MCC codes carry restrictions that go well beyond interchange pricing. Card networks and issuing banks use merchant classification codes to enforce compliance policies, and some codes are treated as high-risk or outright restricted categories. The restrictions are applied programmatically, meaning they trigger automatically based on the code itself, not based on any review of the individual transaction. Cannabis-related businesses, firearms dealers, adult entertainment merchants, and gambling operations all fall under specific MCCs that trigger additional scrutiny. Some issuing banks block transactions to those codes entirely, regardless of the dollar amount or the cardholder's account standing. Others impose enhanced monitoring, lower authorization ceilings, or additional reporting requirements. Card network operating rules, which all processors must follow as a condition of their acquiring agreements, define which MCCs fall into the high-risk tier and what additional due diligence is required. Visa and Mastercard each maintain their own restricted and high-risk MCC lists, and the requirements have tightened over the past several years as regulatory and reputational pressure around certain industries has increased. For merchants in these categories, the MCC designation shapes not just interchange costs but whether they can reliably accept cards at all. These restrictions can also catch businesses that are incorrectly classified. A wellness company coded under a pharmacy or supplement MCC might face transaction blocks intended for a completely different risk profile. A legitimate e-commerce operation coded under a category associated with high chargeback rates might see its authorization approval rate drop with no explanation from the issuing side. The restrictions operate at the network and issuer level, not the processor level. Your processor may not even know why certain cards are declining if the block originates with the cardholder's bank. When MCC Codes Trigger Unexpected Declines Some of the most confusing decline scenarios in payment processing trace directly back to merchant classification. A cardholder's issuing bank may impose spending limits or outright blocks based on the merchant's MCC. Corporate purchase cards are especially prone to this problem. Many corporate card programs restrict transactions to specific MCC categories, so an employee trying to buy office supplies from a business classified under the wrong code will have their card declined at the register with no useful explanation. Government purchase cards follow similar logic. The General Services Administration publishes guidelines specifying which MCC codes are authorized for government purchases, and transactions outside those approved codes are blocked automatically. If your business serves government clients and your MCC doesn't match their approved category list, you'll lose those sales regardless of the product being purchased. These declines don't generate useful error messages. The terminal or gateway typically returns a generic decline code, leaving both merchant and customer without a clear explanation. The merchant can't resolve the issue in the moment because the problem lives in the MCC assignment, which only the acquirer can change. How to Dispute or Change Your MCC Code If you believe your MCC is incorrect, you can request a review. Start with your processor or acquiring bank, since they assigned the code during onboarding. Gather documentation that demonstrates your primary business activity: your business license, a clear description of your products or services, revenue breakdowns if you operate across multiple categories, and your website or marketing materials showing what you actually sell. The acquirer reviews your documentation against the card network's MCC assignment guidelines and can submit a reclassification if the evidence supports it. The timeline varies. Expect anywhere from a few days to several weeks, depending on the processor's internal review process and whether the network requires additional verification. There are limits to what you can request. You can't ask for a specific MCC simply because it carries lower interchange. The code must accurately reflect your primary business activity as defined by the card networks. Networks audit MCC assignments periodically, and a processor that routinely assigns favorable but inaccurate codes risks penalties from Visa or Mastercard. The networks take classification integrity seriously because the entire interchange system depends on merchants being coded accurately. If your processor declines the change and you believe the assignment is wrong, escalating directly to the card network is an option. That path is rarely necessary, though. Most classification disputes resolve at the processor level once supporting documentation is clear and complete. Where to Find the Complete MCC Code List Visa publishes its full MCC code list in the Visa Merchant Data Standards manual, accessible through Visa's business resource portal. Mastercard includes its classification list in the Quick Reference Booklet, which is also publicly available. Both documents are updated periodically as the networks add new codes or reclassify existing ones to reflect changes in how businesses operate and how industries evolve. Third-party reference sites compile these lists into searchable formats, though they don't always reflect the most recent updates. For any classification decision that affects your rates or authorization patterns, the network's own published documentation is the authoritative source. Knowing your MCC code and understanding what it means gives you a practical starting point for conversations with your processor about interchange pricing, authorization patterns, and whether your classification actually matches what your business does. If you're evaluating credit card processing providers, our reviews and comparisons cover how processors handle merchant classification, interchange transparency, and fee structure clarity across the category.

MCC Codes: Merchant Classification and Why It Matters