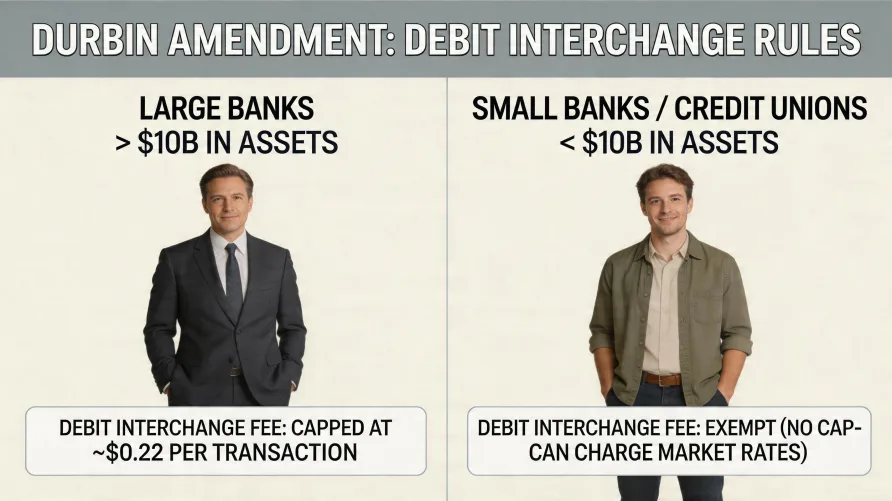

What the Durbin Amendment Actually Does The Durbin Amendment caps how much large U.S. banks can charge merchants in interchange fees on debit card transactions, and it applies only to debit cards issued by banks with $10 billion or more in assets. It doesn't touch credit cards. It doesn't apply to small banks or most credit unions. The cap doesn't directly set what merchants pay overall, just the interchange portion that flows to the card-issuing bank. I've operated and advised on enough merchant accounts over the years to know this single distinction, regulated debit versus exempt debit, drives a meaningful chunk of what appears on a typical small business processing statement. The cap took effect in October 2011 and has stayed largely intact since, though the Federal Reserve proposed lowering it in 2023 and that process is still working through the regulatory pipeline at the time of writing. The official name in regulation is Regulation II, the Federal Reserve's implementing rule for Section 1075 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. Most people in payments call it Durbin after Senator Dick Durbin, who introduced the amendment. How the 2011 Cap Was Built The Federal Reserve's 2011 final rule capped interchange on regulated debit at 21 cents per transaction plus 0.05 percent of the transaction amount, with an optional 1 cent fraud-prevention adjustment for issuers that meet the Fed's fraud-prevention standards. On a $40 grocery purchase, that works out to roughly 24 cents in interchange. Before Durbin, the comparable interchange charge averaged around 44 cents according to Federal Reserve data, so the cut was material. The rule also did something less discussed but arguably just as consequential. It required every debit card carry at least two unaffiliated payment networks, and it gave merchants the right to choose which network routes the transaction. That broke exclusive routing arrangements between issuers and a single network. It opened up routing competition for PIN debit and, eventually after a 2023 Reg II clarification, for card-not-present debit too. The $10 billion asset threshold is what creates the regulated versus exempt split. Big national banks fall above it. Most community banks, regional banks, and credit unions fall below. Cards from exempt institutions don't have a capped interchange rate, and the networks set those rates the same way they always have. That carve-out wasn't an oversight. Congress wrote it into the statute deliberately, on the theory that smaller institutions couldn't absorb the same cost compression as the largest banks without disproportionate harm to community banking. Whether the carve-out actually worked as intended is a separate debate, but the regulatory line itself has stayed in place since 2011 and isn't part of the current Fed proposal to lower the cap. The cap also survived a significant legal challenge early on. A 2014 federal appellate ruling in NACS v. Board of Governors upheld the Fed's interchange cap and routing rules against a merchant-side suit that argued the cap had been set too high. That ruling cemented the 21 cents plus 0.05 percent structure as the operating reality for the better part of a decade. The Two Tiers on Your Merchant Statement If you process a mix of debit cards from a mix of issuers, your statement reflects both tiers. On interchange-plus pricing, you'll typically see line items labeled something like "Regulated Debit," "Exempt Debit," "Regulated Debit CNP" for card-not-present transactions, "Exempt Debit CNP," and similar variants for PIN debit. Each one carries a different interchange rate. Regulated debit interchange runs around 0.05 percent plus 22 cents in most categories. Exempt debit can run anywhere from 0.65 percent plus 15 cents to over 1.6 percent plus 15 cents depending on the network and transaction type, which means the same $50 debit purchase can cost you 25 cents or 95 cents in interchange depending on which bank issued the customer's card. That's a real spread, and there's no setting on your terminal that lets you choose one over the other. Whether the customer pulls out a card from a top-five national bank or a local credit union determines the rate. On tiered pricing the cost difference may be hidden inside qualified versus non-qualified bucket math rather than itemized. The difference matters in concrete numbers. A coffee shop running mostly small-ticket debit transactions ends up with very different effective rates depending on the customer mix. A regulated debit transaction on a $5 sale costs roughly 22 cents in interchange. An exempt debit transaction on the same $5 sale can easily cost 25 to 40 cents. Multiply that gap by thousands of monthly transactions and it adds up. This also explains why processors that quote a single blended "debit rate" or "qualified debit rate" on tiered pricing aren't telling you the full story. The real cost depends on what proportion of your customers swipe regulated cards versus exempt cards, and that mix isn't something you control. How the Cap Affects Small Businesses Small business merchants captured most of the direct interchange savings on the regulated portion of debit volume. That part is uncontroversial. The harder question is what happened on the other side of the equation, and the tradeoffs deserve honest treatment. Banks subject to the cap responded the way you'd expect a regulated industry to respond to revenue compression. Many eliminated or reduced free checking accounts. Monthly account fees rose. Debit rewards programs were cut back significantly. Several Federal Reserve studies and academic analyses have documented these shifts. The broader debate over whether interchange savings actually reached consumers in the form of lower retail prices is still active and probably won't be settled definitively. For a typical small business though, the practical effect is simpler. Your processing costs on debit transactions came down, but only on the share that runs through large-bank cards. If you serve a community where most customers bank locally with smaller institutions, you may have seen less benefit than a merchant in a market dominated by national bank customers. There's no way to predict your exact mix without pulling statement data, and even then it shifts over time as customer banking habits change. Two merchants on identical pricing structures, in identical industries, in cities a hundred miles apart, can end up with measurably different effective debit rates simply because of the local banking footprint. That's an unintuitive outcome of how the law was written, and it's one of the reasons savvy merchants ask their processor for a category-by-category breakdown of debit interchange rather than accepting a blended summary. There's also a payment routing benefit. Because Durbin requires two unaffiliated networks on every debit card, merchants gained the structural ability to route transactions through whichever network offers better economics. Most modern processors handle that routing automatically. But the structural choice exists because of Durbin. Without it, the exclusive single-network routing that existed before 2011 would still be the default. The 2023 Federal Reserve Proposal In October 2023, the Federal Reserve proposed amending Regulation II to lower the cap further. The proposed structure would replace the existing 21 cents and 0.05 percent base with a 14.4 cents and 0.04 percent base, with an updated fraud-prevention adjustment of 1.3 cents. The proposal also introduced a biennial review mechanism that would automatically adjust the cap based on issuer cost survey data going forward. The Fed publishes its biennial debit card issuer cost surveys precisely so the rulemaking record reflects how issuer processing costs have changed over time. According to those surveys, the average authorization, clearance, and settlement cost per regulated debit transaction declined meaningfully between 2009 and 2021. The 2023 proposal's headline numbers were drawn directly from that updated cost data, which is why the proposed base of 14.4 cents sits roughly two-thirds of the existing 21 cent cap. The Fed published the proposal for public comment, and the comment period drew thousands of responses from banks, credit unions, merchant trade groups, and consumer advocates. Banking trade groups argued the lower cap would further compress issuer revenue and could trigger another round of consumer-facing fee adjustments. Merchant groups argued the existing cap is already higher than actual processing costs justify and supported the reduction. As of writing, the proposal hasn't been finalized, and the timing of any final rule remains uncertain. If the proposal is finalized in something close to its current form, regulated debit interchange would drop again, and the savings would flow primarily to merchants on the same regulated-versus-exempt split that already exists. Exempt debit isn't affected by the proposal. Routing Rules and the 2023 Reg II Clarification There's a related rule change that's already in effect and merits attention. In late 2022, the Federal Reserve finalized an amendment to Regulation II clarifying that the two-network requirement applies to card-not-present transactions, not just card-present ones. The amendment took effect July 1, 2023. Practically, online debit transactions now also require routing competition. Issuers were given time to update their cards to comply, and processors had to update their card-not-present routing logic. For merchants, the long-term effect is the same as the original Durbin routing rule. More competition between networks should put modest downward pressure on debit acceptance costs in card-not-present channels over time. This particular change wasn't a new statute or an amendment to Durbin itself. It was a clarifying interpretation of the existing law from the Fed. What Merchants Should Watch For If you're trying to understand what Durbin means for your processing costs in practice, a few things matter more than the regulatory mechanics. Look at your effective rate by debit category. Pull a recent statement and compare regulated debit line items to exempt debit line items. The gap tells you something real about your customer mix and your true debit cost structure. Ask whether your processor passes regulated debit savings through transparently. On interchange-plus pricing, the savings flow through automatically. On tiered pricing, they may or may not, and the answer depends entirely on how the processor structures their qualified, mid-qualified, and non-qualified buckets. This isn't theoretical. It's the single biggest reason interchange-plus tends to outperform tiered pricing for most small merchants. Watch the 2023 proposal's progress. If it's finalized, regulated debit interchange will drop again and your effective rate on that volume should improve, assuming your processor is on interchange-plus pricing. The exact timing depends on when the Fed acts and what implementation period the final rule sets. Don't assume "small bank exempt" means "more expensive than it should be." The exempt designation isn't a regulatory failure. It's a deliberate carve-out, and it's still in place under current law and under the pending proposal. For more on how interchange categories actually shape real processing costs, you can review providers in this market on our credit card processing rankings page, where pricing transparency and statement clarity are scored as part of the methodology.

The Durbin Amendment and Debit Interchange Caps