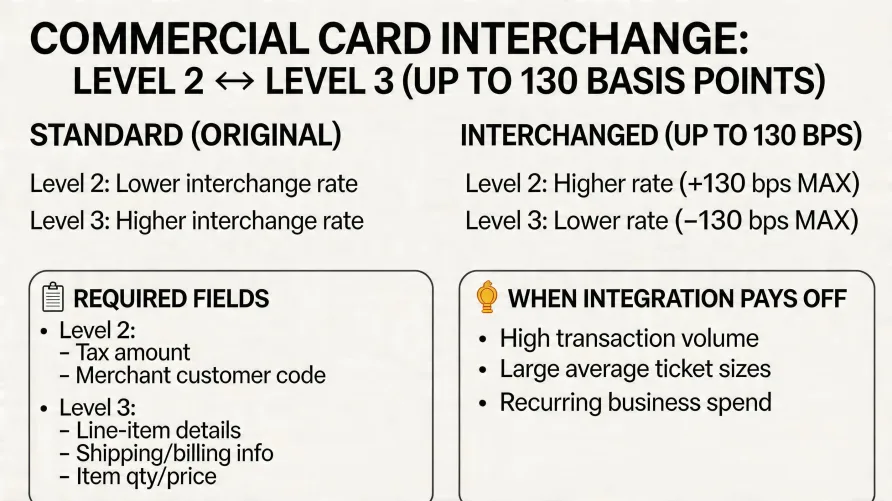

Level 2 and Level 3 credit card processing refers to interchange categories that reduce fees on commercial, corporate, purchasing, and government card transactions when a merchant transmits additional context with the authorization. For B2B merchants, the rate gap between standard interchange and qualified Level 3 can run 80 to 130 basis points. On a million dollars of annual commercial card volume, that translates to $8,000 to $13,000 in direct, recurring savings. What Level 2 and Level 3 Credit Card Processing Actually Mean Card networks publish a tiered interchange schedule. Standard consumer card transactions clear at the highest rates because they carry minimal data, just card number, amount, and merchant identifier. Commercial cards (those issued to businesses, government agencies, and enterprises) qualify for reduced interchange when the merchant submits more transaction context. Visa and Mastercard call these tiers Level 1, Level 2, and Level 3, and each tier requires more data fields than the last. Level 1 is the baseline. Every transaction includes it. Level 2 adds tax amount and a customer reference code. This is the entry point for B2B savings and the most attainable for merchants without heavy technical lift. Level 3 builds on Level 2 with detailed line item data: product descriptions, item quantities, unit prices, commodity codes, freight charges, and shipping origin and destination ZIP codes. Visa's published commercial card interchange tables show the largest reductions sit at Level 3, but qualification rules are stricter and the data requirements are harder to meet. The mechanic isn't that the merchant pays a lower rate as a reward for cooperation. It's that the card-issuing bank can match the transaction against business spend categories for the cardholder's own reporting and reconciliation. The data has economic value to the issuer, so the network passes some of that value back through interchange. Which Cards Qualify for Level 2 and Level 3 Pricing Not every card runs through these tiers. The categories that matter for B2B merchants are commercial credit cards (issued to small and mid-sized businesses), corporate credit cards (issued to mid-market and enterprise companies), purchasing cards or P-cards (issued for procurement and approved spend categories), business debit cards (with limited Level 2 and 3 eligibility that varies by network), and government purchase cards (issued to federal, state, and local agencies under programs like GSA SmartPay). Consumer credit and debit cards don't qualify. Neither do most rewards cards held by individuals, even when used for business expenses. The card BIN, the first six to eight digits, tells the processor which interchange category applies. For a typical merchant, the share of transactions that qualify depends entirely on customer mix. A wholesale distributor selling to procurement departments might see 60 to 80 percent commercial card volume. A B2B SaaS company billing corporate customers might see 40 to 60 percent. A merchant selling to consumers won't see significant Level 2 or Level 3 volume regardless of what data they submit. Required Data Fields for Level 2 Processing Level 2 qualification is the simpler tier. Visa, Mastercard, American Express, and Discover each define their own field requirements, but the common requirements across networks include sales tax amount (typically 0.1 percent to 22 percent of the total, with exempt transactions requiring an explicit flag), customer code or customer reference number (often a PO number or invoice number), tax identification or merchant tax ID depending on the network, and the total transaction amount. Some networks also require destination ZIP code at Level 2. Mastercard's commercial data rate program documentation lists slightly different fields than Visa's, and Amex Level 2 has its own variant. Most modern B2B-capable payment gateways handle the network-specific differences in the background once the merchant turns on Level 2 submission. If sales tax is zero on a particular transaction, the merchant must transmit a tax-exempt indicator rather than just a $0 tax amount. Submitting a $0 tax field without the exempt flag generally disqualifies the transaction from Level 2 rates and the transaction falls back to Level 1. Required Data Fields for Level 3 Processing Level 3 requires everything in Level 2 plus detailed line item data for each item on the invoice. Per Visa's commercial interchange documentation, line item fields include item commodity code (typically a UNSPSC or buyer-specified code), item product code or SKU, item description, item quantity, unit of measure, unit cost, line item discount amount where applicable, line item total, and tax rate and tax amount per line where applicable. Level 3 also adds header-level fields beyond Level 2: ship-from ZIP or postal code, ship-to ZIP or postal code, destination country code, freight or shipping amount, duty amount on international transactions, order date, and order-level discount amount. Visa and Mastercard differ on commodity code requirements. Visa accepts UNSPSC codes (United Nations Standard Products and Services Code). Mastercard accepts UNSPSC and also allows merchant-defined codes in some commercial card programs. Government purchasing programs typically standardize on UNSPSC because federal procurement systems already use it. Data integrity matters as much as data presence. Each line item's quantity multiplied by unit cost, after any discount, must reconcile to the line total. The sum of line totals plus tax and freight must equal the transaction amount within network tolerance. Mismatches generally cause the transaction to fall back to a higher interchange tier even when every required field is technically populated. How Much B2B Credit Card Processing Saves with Level 3 Data The exact savings depend on the card type and the network's published rate for that category, but the general magnitude is consistent. Level 1 to Level 2 typically reduces interchange by 30 to 60 basis points (0.30 to 0.60 percent). Level 2 to Level 3 typically reduces interchange by another 60 to 100 basis points beyond Level 2. The combined reduction from Level 1 baseline to qualified Level 3 often falls between 80 and 130 basis points. These ranges come from card network published interchange tables. Visa and Mastercard update their interchange schedules twice a year (April and October), and the absolute rates shift slightly with each update, but the relative gap between Level 1 and Level 3 has stayed reasonably consistent for over a decade. A practical example using mid-range numbers. A wholesale supplier processes $2 million annually, of which $1.4 million is commercial card volume. Without Level 2 or 3 data, that volume clears at Level 1 commercial rates around 2.65 percent on average. Add Level 2 data and the rate drops to roughly 2.20 percent. Add full Level 3 data and the qualifying transactions drop further to around 1.90 percent. Annual processing cost on that $1.4 million falls from $37,100 to roughly $26,600, a savings of about $10,500 per year. That figure sits at the upper end of typical results. A merchant with smaller average ticket sizes won't see proportional savings because some Level 3 rate categories require minimum transaction amounts (often $1,000 or higher) to qualify for the deepest discounts. Below those thresholds, the rate reduction is smaller though still real. Integration Paths for Submitting Commercial Card Data Fields Three primary paths exist for getting Level 2 and Level 3 data into the authorization message. Payment Gateway Native Support Most established B2B payment gateways support Level 2 and Level 3 fields directly in their API. The merchant or their developer adds the additional fields to the existing authorization call. For Level 2 this is usually a small lift, four or five extra parameters. For Level 3 it's substantially more, because line item data has to be passed as a structured array with each item's full field set. Gateway documentation lists the exact field names, formats, and any network-specific quirks. Some gateways auto-format the data correctly for the relevant network based on the card BIN. Others require the merchant to send network-specific field structures. ERP and Accounting System Integration For merchants whose invoicing already lives in an ERP or accounting system, the line item data needed for Level 3 already exists in structured form. The integration path is to push that data into the payment authorization rather than recreating it. Accounting systems with built-in commercial card processing connectors often handle Level 3 submission automatically when the merchant invoices and accepts payment in one workflow. This is the cleanest path for merchants doing volume. The data is already structured, already accurate, and already reconciles. The development work is mapping the ERP fields to the gateway's Level 3 schema once. Manual Keyed Entry For low-volume merchants or one-off transactions, some virtual terminals offer manual Level 2 and Level 3 entry. The merchant types in line items, tax, freight, and customer code at the time of capture. This works but doesn't scale. Keying errors will cause downgrades, and the time cost per transaction generally outweighs the savings unless the average ticket is several thousand dollars. When Level 3 Processing Pays Off, and When It Doesn't The integration work to support Level 3 isn't trivial. Run the math before committing. The rough breakeven calculation: take the percentage of qualifying commercial card volume, multiply by the Level 3 versus Level 1 rate gap (use 100 basis points as a working estimate), and apply that to annual revenue. If the resulting savings exceed development and ongoing maintenance cost over two years, Level 3 is probably worth pursuing. Some scenarios where Level 3 makes clear economic sense include wholesale and distribution businesses with high commercial card volume and average tickets above $500, B2B SaaS companies billing corporate customers via commercial cards on annual or semi-annual contracts, government contractors accepting GSA SmartPay or state purchasing cards, and manufacturing or industrial suppliers selling into procurement departments. Some scenarios where it usually doesn't pay off include merchants with under $250,000 in annual commercial card volume (the absolute savings rarely justify the integration), merchants with average tickets under $50 (the Level 3 rate categories favor larger transactions), merchants whose customers pay primarily by ACH, wire, or check rather than card, and merchants whose card volume is mostly consumer rewards cards that don't qualify for commercial interchange at all. A useful intermediate position exists. Implement Level 2 only. The data requirements are minimal, most B2B-capable gateways handle it with a few configuration changes, and the rate reduction captures roughly half of the total available savings. Level 2 alone often pays for itself within a quarter for any merchant with meaningful B2B volume. Do You Need Special Software for Level 3 Processing In most cases the answer is yes, but not new software. The existing payment gateway handles Level 2 and Level 3 transmission if it's a B2B-oriented gateway. The merchant or their developer turns the feature on and configures field mapping. For merchants on consumer-focused gateways, switching to a B2B-capable gateway may be the prerequisite. ERP and accounting systems that support commercial card processing often include Level 2 and Level 3 submission as a built-in feature. The merchant doesn't write integration code in those cases, but configuration is still required to make sure the right fields populate from invoice data. For merchants without an ERP and without development resources, hosted virtual terminals with manual Level 3 entry exist but aren't a practical long-term solution at any meaningful volume. What to Verify Before Switching Processors for Level 3 Switching processors specifically to access Level 3 pricing is reasonable, but the savings only materialize if the new processor actually passes through the lower interchange. Some processors charge flat rates regardless of interchange tier, which means Level 3 data submission doesn't reduce the merchant's effective cost even though the underlying interchange falls. Three things to verify before signing. The processor must use interchange-plus pricing, not flat-rate or tiered pricing. The processor's gateway must support the Level 3 fields the merchant needs to submit. And the processor's monthly statements must break out interchange separately so the merchant can verify the rate reductions actually flow through to the bottom line. Interchange-plus pricing is the structure that makes Level 3 economics work. Under this model the merchant pays the actual interchange rate plus a fixed processor markup. When interchange drops because of Level 3 data, the merchant's cost drops with it. Under flat-rate or tiered pricing, the processor captures the savings and the merchant sees no benefit. Final Considerations for B2B Merchants For B2B merchants doing real commercial card volume, Level 2 and Level 3 processing is one of the higher-impact cost reductions available. The mechanics aren't intuitive, the data requirements are exacting, and the integration takes effort, but the savings are real and recurring once the work is done. The order of operations that works for most merchants: start with a processor that supports interchange-plus pricing and has a B2B-capable gateway, implement Level 2 first because it's quick and captures meaningful savings, then implement Level 3 for the transaction segments where line item data is readily available from an ERP or invoicing system. For a look at providers in this market and how they compare on commercial card support, pricing structure, and Level 2 and 3 capabilities, see our credit card processing rankings.

Level 2 and Level 3 Data: How B2B Merchants Unlock Lower Rates