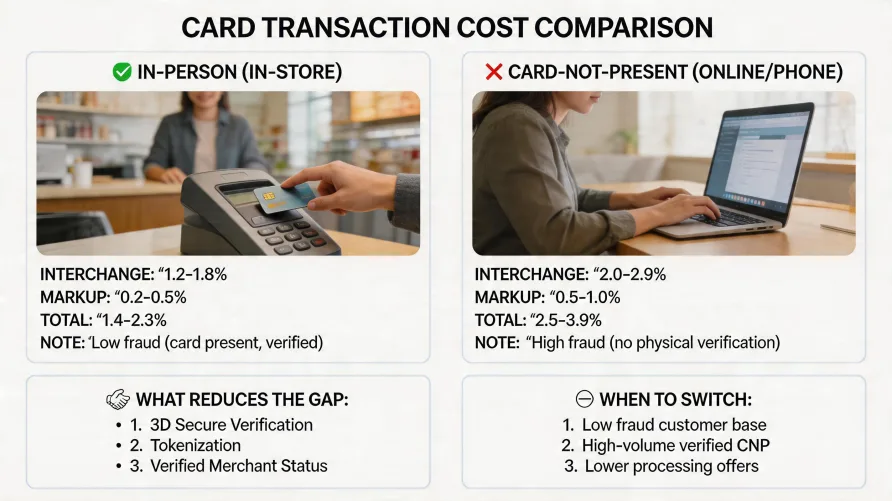

The gap between card-not-present vs card-present fees usually lands between 30 and 50 basis points at the interchange layer, with processor markup adding more on top. For a merchant running $50,000 a month in card volume online versus in person, that's roughly $150 to $250 disappearing into processing costs every month, and that's before keyed transaction downgrades make the math worse. After 20 years of helping operators read their own statements, I keep seeing the same pattern: merchants know online costs more, but they have no idea by how much, why, or what they can do about it. This is fixable. Most of the gap comes from interchange rules set by the card networks, but a real chunk lives in the rate categories your transactions land in, and those are partially under your control. Why Card-Not-Present Fees Run Higher The card networks price interchange around fraud exposure. When a chip card is dipped or tapped at a terminal, the chip authenticates the card to the issuer in real time, and the issuer accepts a larger share of fraud liability if something goes wrong. The merchant did everything the network rules require. When that same card number is typed into a checkout form online or read off a phone over the counter, the chip never wakes up. The merchant has the digits. That's it. There's no way to confirm the card is real, the cardholder is the actual person, or the order isn't a stolen number being burned through before the next chargeback hits. The issuer is the party stuck holding the loss when fraud succeeds, and the networks build that risk back into the interchange rate every CNP transaction pays. The merchant doesn't see this calculation on a statement, but it's the central reason an online sale costs more than the same sale across a counter. Visa and Mastercard publish separate interchange categories for the two scenarios. A standard retail credit transaction with a chip read tends to land in the lowest cost tier the network offers for that card type. The same card, same purchase, processed online with full address verification and a CVV match, lands in a tier that's typically 20 to 35 basis points higher. A keyed transaction without verification lands higher still. The Federal Reserve has documented interchange rate structures across both debit and credit in its public data collections. The card networks themselves publish their interchange tables, and any processor will furnish them on request. The risk-based logic isn't hidden. Fraud rates on card-not-present transactions run several times higher than card-present, and the rate tables exist to compensate the issuer banks for that exposure. The Markup Layer Compounds the Interchange Gap Interchange is only the first piece of the bill. The processor adds markup on top, and that markup tends to run higher on CNP volume because the underwriting risk profile differs. Aggregators that quote a single flat rate, like 2.9% plus 30 cents for online transactions, are blending the higher CNP interchange and a margin that absorbs chargeback risk into one published number. It looks simple. It's also expensive once you run annualized math against an interchange-plus alternative, especially for merchants doing more than $25,000 to $30,000 in monthly card volume. On a tiered pricing plan, CNP volume usually drops into the "mid-qualified" or "non-qualified" tier automatically, regardless of whether the transaction actually triggered any real downgrade condition. That's a statement structure problem more than a fraud problem. Tiered processors choose where to bucket transactions, and CNP almost always lands in a more expensive bucket by default. You can ask for the actual interchange categories your transactions are landing in. Most merchants never do. Is Keyed Entry More Expensive Than Online Processing? This catches more merchants off guard than any other charge on a processing statement. A retail merchant with a physical terminal assumes they're being billed at card-present rates. Then a customer's chip card won't read, the cashier types the number in, and that one transaction gets billed as if it were an online purchase. Keyed transaction rates are usually identical to online rates, sometimes worse. The networks treat keyed entry on a physical terminal as card-not-present because the chip never authenticated. Same fraud risk, same interchange tier. For a merchant doing even 5% of their transactions as keyed entries, the cumulative cost over a year is real money. I've reviewed statements where a small business was paying 50 to 80 basis points more than they thought, simply because their staff defaulted to keying in cards instead of asking customers to insert or tap. How to Lower Your Card-Not-Present Processing Rates CNP processing rates aren't fixed. Card-not-present transactions can qualify for better interchange categories if you supply more verification data with each authorization. The network rules reward merchants who reduce the issuer's fraud exposure, and the savings show up at the interchange level, not just in markup negotiation. These are the levers that actually move the rate. Address Verification Service (AVS) AVS sends the cardholder's billing zip code or full street address to the issuer for confirmation against the card on file. A full match qualifies a CNP transaction for a better interchange tier. A partial match is better than no match. No AVS data at all almost guarantees a downgrade. Any modern gateway supports AVS, but plenty of merchants disable it because of false declines on international orders. Tightening fraud rules typically pays for itself. CVV Verification The three or four digit code on the back of the card (CID, CVV2, or CVC2 depending on the network) confirms the person ordering at least had the physical card in hand at the moment of purchase. PCI rules prohibit storing CVV after authorization, which means a stolen database of card numbers won't include it. CVV match on a CNP transaction is another lever for qualifying for the better interchange categories. 3D Secure (Visa Secure, Mastercard Identity Check) EMV 3-D Secure is the modernized version of the older 3DS protocol, with specifications published by EMVCo. It runs an authentication step between the cardholder and the issuer at checkout, often invisible to the customer if the issuer's risk model is satisfied. The bigger benefit isn't friction reduction. It's a liability shift. When a 3DS-authenticated transaction is later disputed as fraud, the chargeback liability moves from the merchant to the issuer in most cases. Lower fraud loss plus better interchange treatment makes 3DS a strong tool for any e-commerce merchant doing real CNP volume. Tokenization Tokenization replaces the actual card number with a non-sensitive token at the point of capture, so the real number never touches your systems. The PCI Security Standards Council has published guidelines on network tokenization, where the issuer or the card network mints the token. Network tokens carry their own interchange benefits in many cases, plus they reduce PCI scope and improve authorization rates on stored credentials. Card-on-file merchants and subscription businesses see the most direct rate benefit here. Recurring and Installment Indicators If your business charges customers on a regular schedule, flag those transactions properly with the recurring transaction indicator. The same applies to installments, deferred billing, and unscheduled credentials-on-file charges. Each scenario has its own message field on the authorization, and each has its own interchange category. Sending a recurring charge as a one-time CNP transaction means paying a higher rate and accepting more authorization declines than you should. Settle Within 24 Hours Authorizations not settled within a defined window get downgraded automatically. The exact window varies by card type and network rules, but in most cases batching out at the end of every business day prevents the most common downgrade. If your gateway is set to manual capture, verify the timing matches network requirements for your typical order flow. When You Can Move Volume to Card-Present (and When You Can't) Some businesses take both online and in-person payments. A specialty retailer with an e-commerce site, a service business with a phone-order option and a storefront, a contractor who can either invoice or close on site. For these merchants, the rate gap between online vs in person processing fees is reason enough to make in-person the default whenever possible. Mobile readers attached to phones now make card-present capture practical for field service, mobile vendors, contractors, and event-based businesses. A real card-present read with a tap or a chip dip qualifies for the lowest interchange tier the card type supports, even if the merchant has no fixed location. That's a real rate improvement over keying the same number into a payment link sent by text. But not every business has the choice. Pure e-commerce, subscription services, telephone order takeoff, mail order, and any B2B operation invoicing on net terms will run CNP volume by definition. The right move there isn't to pretend the volume can be moved. It's to make sure every CNP transaction is sending the maximum verification data the networks reward. The Bottom Line on Online vs In-Person Processing Fees The card-not-present vs card-present fee gap is real and it's permanent. The networks won't price it out. What you can control is how many transactions get downgraded inside that gap and how much markup your processor adds on top. For most merchants I've reviewed, the highest-impact moves are turning AVS and CVV on, evaluating 3DS for e-commerce, properly flagging recurring transactions, and training counter staff to never key in a card if a chip read is available. Those changes don't require a new processor. They require a few hours with your gateway settings and a careful read of your next statement. If your processor refuses to give you a breakdown of which interchange categories your transactions are landing in, that's a signal in itself. Transparent processors will hand it over. Opaque ones bank on the fact that most merchants never ask. If you're shopping for a processor that handles CNP volume well, the providers in this market vary widely on transparent pricing, gateway capability, and the actual interchange categories your transactions land in. Our credit card processing rankings cover what each provider offers and where they fit best.

Card-Not-Present vs Card-Present: The Real Rate Difference