Why Shopify Merchants Pay Less for Credit Card Processing

Every Shopify merchant who uses a third-party payment gateway pays an extra surcharge on top of their processor's fees. On the Basic plan, that surcharge is 2% of every transaction. On the Grow plan, it's 1%. On Advanced, 0.6%. These aren't credit card processing fees from Visa or Mastercard. They're fees Shopify charges you for the privilege of not using Shopify Payments. For a store processing $10,000 a month on the Basic plan, that's an extra $200 gone before your actual card processing costs even enter the picture.

Shopify Payments eliminates that surcharge entirely. It's built directly into the platform, powered by Stripe's infrastructure on the back end, and managed from the same admin dashboard where you handle orders, inventory, and shipping. We score Shopify Payments 8.0 out of 10 for the credit card processing category. Shopify Inc. (NYSE: SHOP), founded in 2006 by Tobias Lütke and headquartered in Ottawa, Ontario, now powers more than 4.8 million stores across 175+ countries, with merchants generating over $292 billion in gross merchandise volume in 2024 alone. That scale matters because it means the payment infrastructure has been stress-tested at volumes most processors never touch.

How Shopify Credit Card Processing Actually Works

Activating Shopify Payments takes about two minutes. You don't fill out a separate merchant account application or wait for underwriting approval. From your Shopify admin, you go to Settings, click Payments, and turn it on. Your store immediately accepts Visa, Mastercard, Discover, American Express, and Apple Pay. That's it.

Behind the scenes, Shopify Payments runs on Stripe's processing network, which handles the actual card authorization, settlement, and fraud screening. You don't interact with Stripe directly, though. Everything lives inside Shopify's admin: transaction history, payout schedules, chargeback management, and analytics. When a customer buys something, the funds flow through Shopify's system and land in your bank account on a rolling schedule, typically every two to three business days.

The integration advantage goes deeper than just accepting cards. Because Shopify Payments is native to the platform, your order data, payment data, and customer data all live in one place. There's no reconciliation between a payment gateway dashboard and your Shopify admin. Refunds process with a click, and the financial reports in Shopify automatically reflect every transaction without manual syncing. For merchants running both an online store and physical retail through Shopify POS, in-person and online sales consolidate into a single view. That unification is where Shopify Payments creates the most operational value, particularly for stores managing high order volumes across multiple channels.

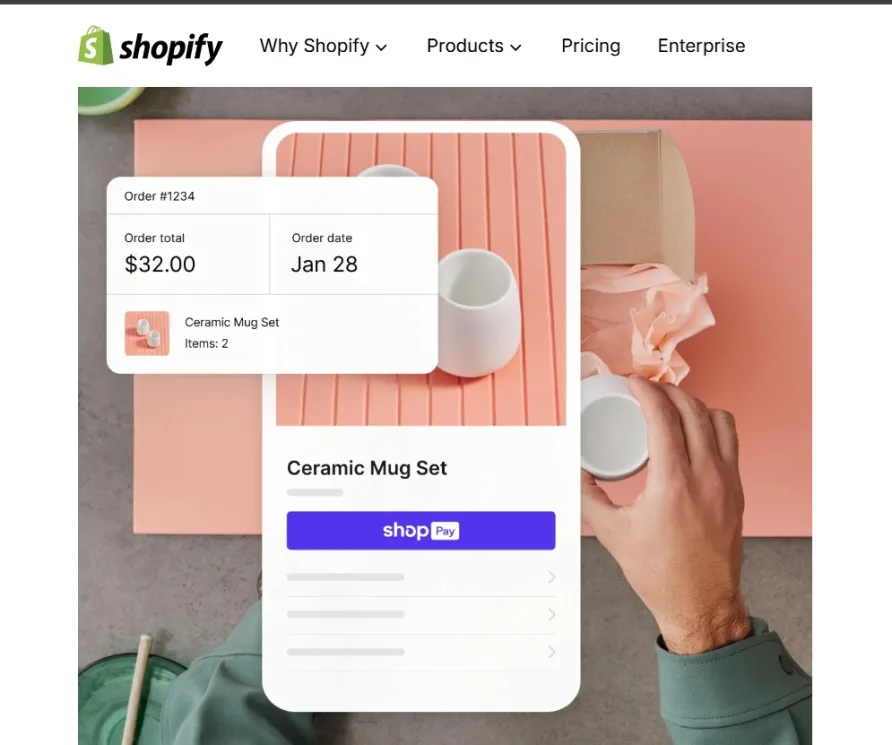

Shop Pay, Shopify's accelerated checkout, deserves specific attention here. With over 150 million users globally, Shop Pay stores customer shipping and payment details for one-tap future purchases. An external study by a major global consulting firm found that Shop Pay lifts checkout conversions by up to 50% compared to guest checkout and outperforms other accelerated checkout options by at least 10%. During the 2024 Black Friday/Cyber Monday weekend, Shop Pay usage surged 58% year-over-year. Even when a customer doesn't use Shop Pay, its mere presence on the checkout page increases lower-funnel conversions by 5%, according to Shopify's data.

What Shopify Payments Costs (and What You Actually Save)

The savings math is the real story here, not just the published rates. A merchant on the Basic plan using a third-party processor like Stripe directly would pay Stripe's standard 2.9% + 30¢ per transaction, plus Shopify's 2% surcharge. On a $50 order, that's $1.75 to Stripe and $1.00 to Shopify, for a total of $2.75. With Shopify Payments, that same order costs $1.75 total. The surcharge disappears.

Processing rates scale with your Shopify plan tier. All rates below reflect monthly billing:

On the Basic plan ($39/month), online transactions cost 2.9% + 30¢ and in-person transactions run 2.7% with no per-transaction flat fee. The Grow plan ($105/month) drops online rates to 2.6% + 30¢ and in-person to 2.5%. Advanced ($399/month) brings online rates down to 2.4% + 30¢ and in-person to 2.4%. Shopify Plus merchants negotiate custom rates. Annual billing reduces the subscription cost significantly: $29, $79, and $299 per month, respectively.

Here's what those rates mean in practice. A solo merchant on the Basic plan processing $8,000 per month in online sales pays roughly $262 in processing fees monthly, or $3,144 annually, plus $468 for the subscription on annual billing. A five-person operation on the Grow plan processing $40,000 monthly pays about $1,160 in processing fees, or $13,920 annually, plus $948 for the annual subscription. That Grow-plan merchant saves approximately $4,800 per year in third-party gateway surcharges alone compared to using an external processor. The subscription cost difference between Basic and Grow is $480 per year, which means the lower processing rates pay for the upgrade once monthly volume crosses roughly $15,000.

Chargebacks carry a $15 fee, refunded if you win the dispute. International and American Express transactions may incur higher rates. Currency conversion adds a 1.5% fee when you accept payment in a currency different from your payout currency.

Who Should Use Shopify Payments

The clearest case is straightforward: if you already run a Shopify store, using anything other than Shopify Payments costs you money. The third-party surcharge alone makes the decision for most merchants.

Consider a home goods brand running a Shopify store with both an online presence and a weekend pop-up market. With Shopify Payments, the owner processes online orders and in-person sales through the same system. When a customer buys a candle at the Saturday market, that transaction shows up alongside the Tuesday night website order in the same dashboard. Inventory adjusts automatically. The owner doesn't reconcile between two payment systems at the end of the month. For businesses operating across online and physical channels, this consolidation removes a real administrative burden that dedicated processors can't match for Shopify stores.

The fit weakens for two types of merchants. First, businesses in industries Shopify considers high-risk, including CBD, supplements, firearms, and adult products, may find their accounts flagged, funds held, or Shopify Payments terminated entirely, even if the products are legal. Users in these categories consistently report unexpected fund freezes with limited communication from Shopify during the review process. A merchant selling legal CBD products who scales quickly through a viral marketing campaign could face weeks of frozen payouts while Shopify's risk team reviews the account. Second, merchants operating in countries where Shopify Payments isn't available have no choice but to use a third-party gateway and absorb the surcharge.

Where Shopify Payments Falls Short

The most persistent criticism involves fund holds. Because Shopify Payments operates as a payment aggregator (your transactions process under Shopify's master merchant account, not your own), the platform can freeze payouts when its risk algorithms detect anomalies. Sudden sales spikes, rising chargeback rates, or compliance questions can trigger a hold. Users managing seasonal businesses or running promotional campaigns report payouts frozen for days or weeks, sometimes with minimal explanation. This isn't unique to Shopify. It's inherent to the aggregator model. But for a merchant whose cash flow depends on predictable access to revenue, the experience is disruptive.

Customer support has declined. Shopify discontinued phone support in spring 2025, routing merchants to AI chatbot triage before reaching a human agent via chat or email. Long-term users consistently note that resolving payment-specific issues, particularly fund holds, takes longer than it did when phone support existed. A recurring theme in feedback from established merchants is frustration with having to convince a chatbot to escalate an urgent payment issue to a live representative.

Shopify Payments only works on Shopify. That's obvious, but it carries an implication: your payment processing is locked to your platform. If you ever migrate away from Shopify, you lose your processor, your transaction history, and your Shop Pay checkout optimization. For merchants evaluating Shopify Payments, this isn't a flaw so much as a commitment to acknowledge. You're choosing convenience and savings in exchange for platform dependency.

Recent Shopify Payments Updates

Shopify's Summer 2025 Editions release brought several meaningful changes. Shopify Payments expanded to 16 new countries, bringing the total to over 23 markets with native processing. The same release introduced multi-entity selling, allowing Shopify Plus merchants to process transactions from multiple business entities within a single store, each with its own domestic card processing and local currency payouts. This is a significant operational improvement for brands selling across legal entities in different countries.

AI-powered fraud prevention is now integrated directly into the checkout flow, screening transactions in real time before they complete. The Winter 2026 edition improved chargeback rate tracking with more granular metrics, giving merchants better visibility into dispute patterns. Tap to Pay expanded to additional countries on both iPhone and Android, reducing the hardware barrier for in-person selling. Klarna, built into Shopify Payments, rolled out to 11 additional European countries for installment payments.

Our Assessment

If your business runs on Shopify, Shopify Payments is the default choice for a reason. The elimination of third-party surcharges, the unified dashboard, and Shop Pay's conversion advantages create a cost and operational benefit that standalone processors can't replicate within the Shopify ecosystem. For the typical Shopify merchant processing between $5,000 and $50,000 per month, the annual savings in eliminated surcharges and reduced processing rates at higher tiers add up to thousands of dollars.

The trade-offs center on control and flexibility. You're processing under an aggregator model that can freeze your funds with little warning. You're tied to a platform with declining support responsiveness. And you're making a commitment: if Shopify ever stops being the right e-commerce platform for your business, your payment processing goes with it. For most Shopify merchants, those trade-offs are worth accepting. For merchants in high-risk categories or those who need processor independence, a dedicated merchant account with a third-party Shopify-compatible gateway remains the safer path.